Understanding retirement account options for small business owners is essential in today’s economic landscape. As an entrepreneur, it’s not just about ensuring a comfortable retirement for yourself—it’s also about offering compelling benefits to your team. With an array of retirement account options available, each with unique advantages, choosing the right one can set the foundation for financial success.

In this guide, we’ll unravel the complexities of each retirement account type, from the well-known IRAs to the more intricate SEP IRAs, SIMPLE IRAs, Solo 401(k)s, and Defined Benefit Plans. Our goal is to provide you with the knowledge to select the best small business retirement account that aligns with your financial objectives and long-term business goals.

Traditional IRA: A Starter Retirement Account Option for Small Business Owners

Basics and Benefits: The Traditional IRA is a fundamental retirement account option for small business owners. The contributions you make are typically tax-deductible, reducing your taxable income for the year the contributions are made. The funds in your IRA grow tax-deferred until you withdraw them in retirement.

Contribution Limits and Tax Implications: For 2023, the contribution limit for a Traditional IRA is $6,500, with an additional $1,000 allowed as a “catch-up” contribution if you’re over 50. The deductibility of these contributions can be limited if you or your spouse are covered by a retirement plan at work and your income exceeds certain levels.

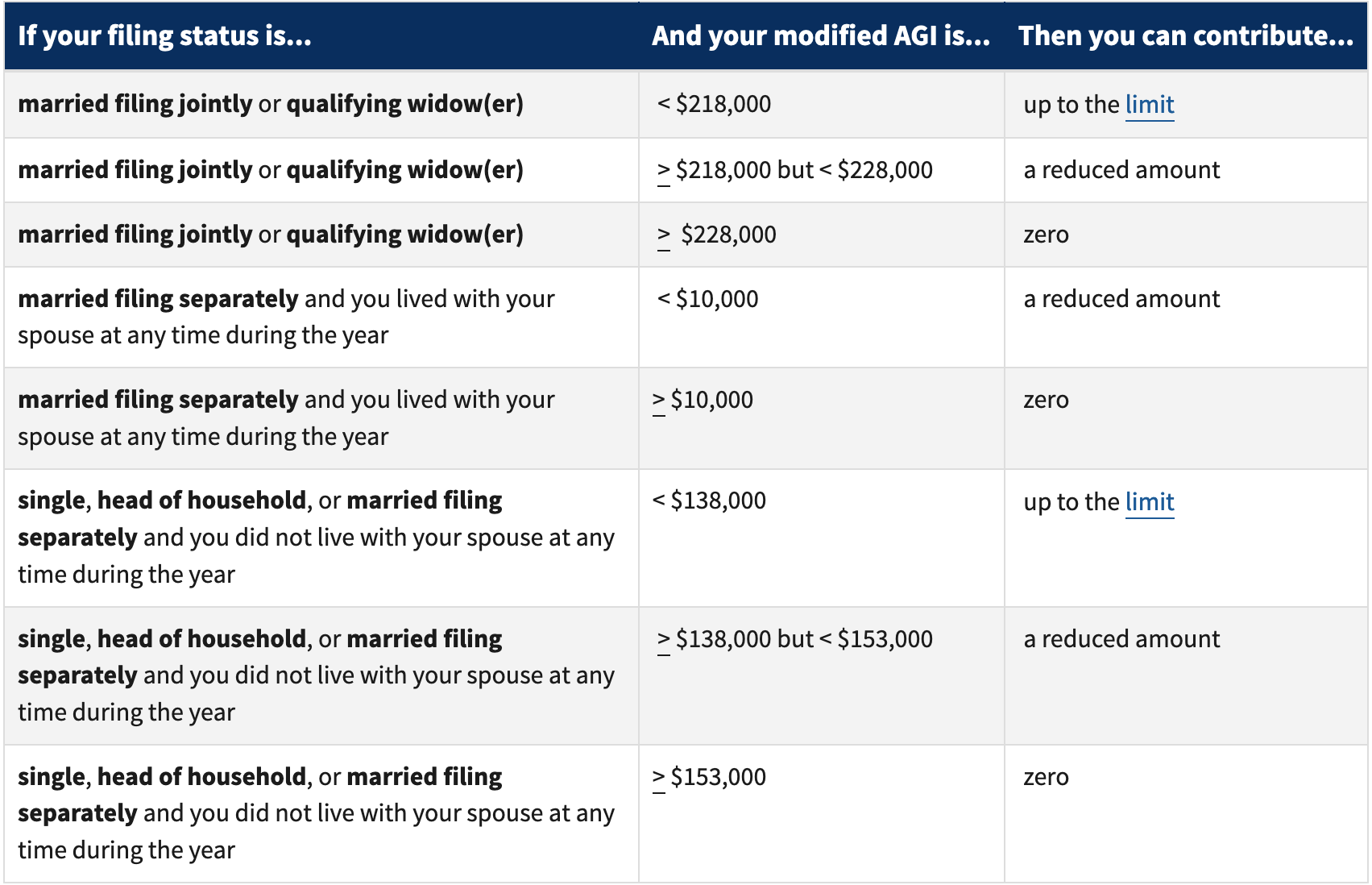

Roth IRA: The Future-Focused Retirement Account Option for Small Business Owners

Difference from Traditional IRA: Unlike a Traditional IRA, contributions to a Roth IRA are made with after-tax dollars. This means you don’t get a tax deduction upfront, but qualified withdrawals in retirement are tax-free, including the earnings on your investments.

This can be particularly advantageous if you expect to be in a higher tax bracket in retirement or if you want to leave tax-free money to your heirs.

Qualifications and Benefits: The Roth IRA stands out among retirement account options for small business owners by offering tax-free growth and withdrawals, provided certain conditions are met.

For 2023, the contribution limit for a Roth IRA is $6,500, with an additional $1,000 allowed as a “catch-up” contribution if you’re over 50. However, there are income limits that apply when contributing to a Roth IRA, which begins to phase out at higher income levels.

Source: IRS

SEP IRA: The Simplified Retirement Account Option for Growing Small Businesses

Suitability for Small Businesses: SEP IRAs are a popular retirement account option for small business owners due to their high contribution limits and straightforward administration.

Contribution Rules and Limits: One of the most significant benefits of a SEP IRA is the high contribution limit – up to 25% of each employee’s pay or $66,000 for 2023, whichever is less. Employers make all contributions, which are tax-deductible, and employees are immediately 100% vested in all SEP IRA contributions.

Note: Employees, not the employers manage the investment decisions in their respective SEP IRA accounts.

SIMPLE IRA: A Collaborative Retirement Account Option for Small Business Teams

Comparison to SEP IRA: The SIMPLE (Savings Incentive Match Plan for Employees,) IRA is designed for businesses with 100 or fewer employees. It’s also conducive to encouraging employee contributions, unlike the SEP IRA, which is employer-funded.

Eligibility and Contribution Matching: Employers must either match employee contributions dollar for dollar up to 3% of their compensation or contribute 2% of each eligible employee’s compensation. The contribution limit for a SIMPLE IRA in 2023 is $15,500, with a catch-up contribution of $3,500 for those over 50.

Solo 401(k): The Dual Benefit Retirement Account Option for Solo Entrepreneurs

How It Works for Sole Proprietors: Unique among retirement account options for small business owners, the Solo 401(k) plan allows you to wear two hats: you can contribute as both the employer and the employee, maximizing retirement contributions and tax benefits.

Contribution Limits and Tax Advantages: The total contribution limit for a Solo 401(k) in 2023 is $66,000, or $73,500 if age 50 or older, which includes both employee deferrals and employer contributions. This plan can also allow for loans and Roth contributions, though the latter does not provide upfront tax deductions.

Defined Benefit Plans: The Structured Retirement Account Option for Small Business Owners

Traditional Pension Plans for Small Business Owners: Defined Benefit Plans are less common but can be advantageous for high-earning business owners who want to save a lot for retirement in a short amount of time. The company is responsible for managing the plan’s investments and risk and will usually hire an outside investment manager to do this.

Long-term Benefits and Considerations: They promise a set annual benefit upon retirement, which requires actuarial calculations and can be more complex to manage. The funding requirements are typically higher than other plan types, but the potential tax-deferred savings are also more significant.

However, poor investment returns can result in a funding shortfall, where employers are legally obligated to make up the difference with a cash contribution.

Profit-Sharing Plans: Profit-Sharing Plans: The Flexible Retirement Account Option for Profitable Small Businesses

How They Can Be Structured: As a retirement account option, Profit-Sharing Plans give small business owners the flexibility to contribute varying amounts year to year, based on profitability.

Tax Benefits and Contribution Flexibility: Contributions are discretionary and tax-deductible, up to the lesser of 25% of compensation or $66,000 for 2023. This type of plan also allows for a vesting schedule, which can incentivize employees to stay with your company longer.

403(b) Plans: A Purpose-Specific Retirement Account Option for Non-Profit Small Businesses

Specifics for Non-Profit Organizations: Similar to a 401(k), a 403(b) is designed for employees of tax-exempt organizations. It allows employees to make pre-tax contributions through salary deferrals.

Comparison to Other Retirement Accounts: Like a 401(k), employees may be eligible for employer matching, and the plan may offer loan provisions and hardship withdrawals. The contribution limits are the same as a 401(k), with the added benefit of a “15-year rule” that allows certain long-tenured employees to make additional contributions.

Health Savings Account (HSA): An Unconventional Retirement Account Option for Small Business Owners

The Dual Role of HSAs: HSAs are not just for medical expenses; an HSA can be a strategic retirement account option for small business owners.

Contributions are made with pre-tax dollars, grow tax-free, and can be withdrawn tax-free for qualified medical expenses. After age 65, funds can be withdrawn for any purpose without penalty, although they may be subject to income tax if not used for medical expenses.

Long-term Benefits for Healthcare in Retirement: As healthcare costs can be a significant expense in retirement, an HSA serves as a strategic reserve for future medical expenses, offering triple tax advantages that are unparalleled by other retirement accounts.

By understanding the nuances of each retirement plan, you can choose the best small business retirement account that caters to your individual needs and business goals. With careful planning and a strategic approach, you can build a robust financial foundation that supports you and your employees well into the future.

If you have questions about your current plan or need help setting one up, feel free to contact us.