In the age of personalized medicine, tailored education, and customized diets, isn’t it time we started considering a personalized approach to inflation?

Inflation, as any economist will tell you, is the general rise in prices and the concurrent decrease in purchasing power over a period of time.

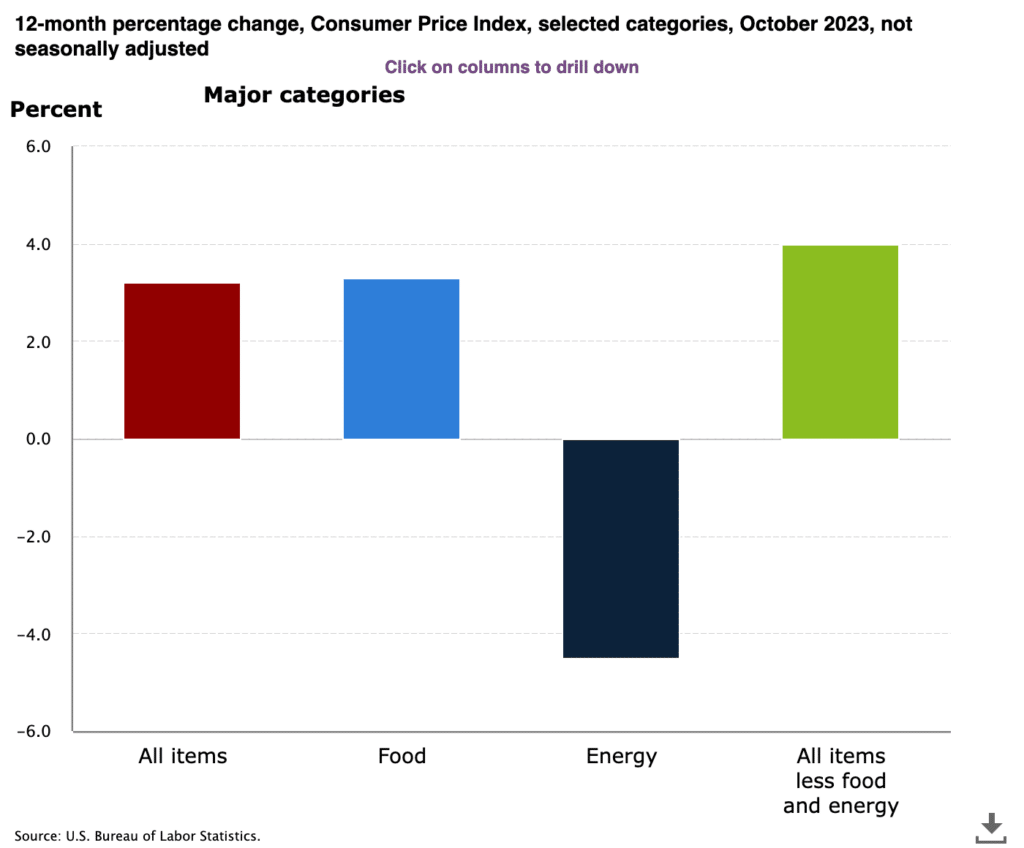

Most countries have an official inflation rate that’s primarily based on the Consumer Price Index (CPI). But what if the generalized CPI doesn’t quite match with your personal spending habits?

Why the Need for Personalized Inflation Rate?

Why the Need for Personalized Inflation Rate?

For most people, the headline inflation number is a good starting point. It gives a general sense of how prices are changing for a broad basket of goods and services. But, not everyone spends money in the same way or on the same things.

A retiree might spend more on healthcare, while a young family might focus on education and childcare. These categories can have widely differing inflation rates.

Therefore, relying solely on the CPI can lead to miscalculations in one’s financial planning.

Determining Your Personalized Rate

To determine a personalized inflation rate, one must start by analyzing their personal spending habits.

Some steps to follow include:

- Track Your Spending: Before understanding your inflation rate, you need a clear view of where your money goes. Categorize your expenses, like housing, food, transport, education, health, entertainment, etc.

- Compare to the CPI: Once you have a clear understanding of your personal expenses, check how each category is weighted in the official CPI.

- Calculate Weighted Inflation: If you find that your spending doesn’t align with the CPI weights, recalculate inflation using your personal weights for each category. If education makes up a larger portion of your budget, and it’s experiencing a higher inflation rate, then your personal inflation might be higher than the official rate.

- Adjust Regularly: Your spending patterns and priorities will change over time. Maybe you’ll buy a house, have children, or retire. These changes will influence your personalized inflation rate.

Benefits of a Personalized Rate

The price of consumer items can rise faster than inflation

- More Accurate Financial Planning: Knowing your personalized inflation rate can make your financial projections more accurate. If your personal inflation is higher than the general rate, you might need to save more for future expenses or retirement.

- Targeted Investment: If certain categories in your budget are experiencing higher inflation, you might consider investing in assets that hedge against that specific inflation. For example, if healthcare costs are rising, investing in healthcare stocks might be a smart move.

- Personal Empowerment: Being aware of your own inflation rate empowers you to make informed decisions and adjustments to your lifestyle, spending, and investment strategies.

Working with Financial Advisors

It’s important to note that while you can estimate your personalized inflation rate, it’s beneficial to engage a financial advisor in this process. They can provide valuable insights, tools, and resources to ensure that your calculations are accurate and that your investment decisions are sound.

A personalized inflation rate provides a more granular view of how rising costs are impacting your specific lifestyle and needs. By tailoring this rate to your individual circumstances, you can make more informed decisions about your financial future, ensuring that your savings, investments, and financial plans are on track to meet your unique goals and requirements.