Recent reports that the Social Security trust fund will pay out more than it takes in—for the first time since 1982—could trigger a rush to claim benefits. Financial planners say that often their clients want to sign up for Social Security at age 62 (the earliest they can file) because they fear that the money won’t be there for them if they wait.

Long-Term Outlook

The long-term outlook for Social Security may be cloudy, but this much is clear: Claiming early could do far more damage to your long-term financial security than anything that happens in Washington.

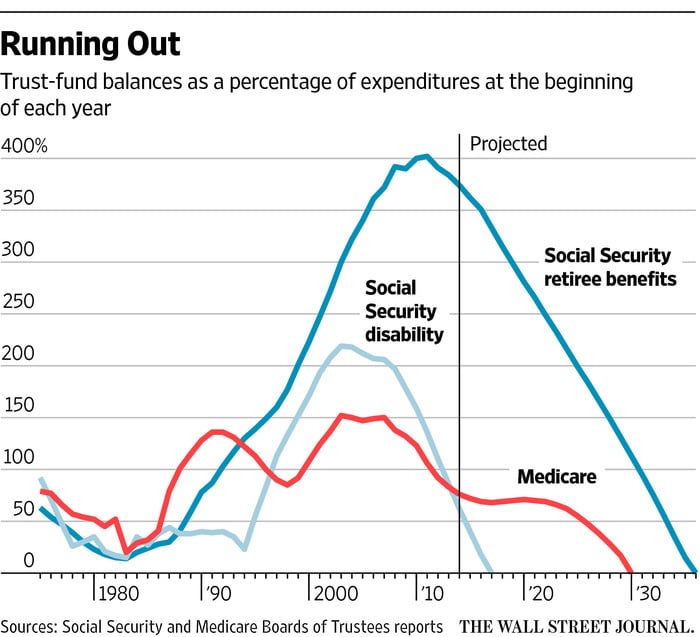

The Social Security Board of Trustees will begin tapping its nearly $3 trillion trust fund to cover payouts this year. If Congress takes no action, the trust fund is projected to run out of money in 2034.

Even if that happens, Social Security benefits won’t disappear. There will still be enough money from payroll taxes to pay 79% of promised benefits.

But it’s unlikely that Congress will do nothing over the next 16 years to fix the program. “Any politician who will not vote to fully support Social Security will not win an election,” says David Offenberg, associate professor of finance at Loyola Marymount University.

Social Security Has Been in Worse Straits Before

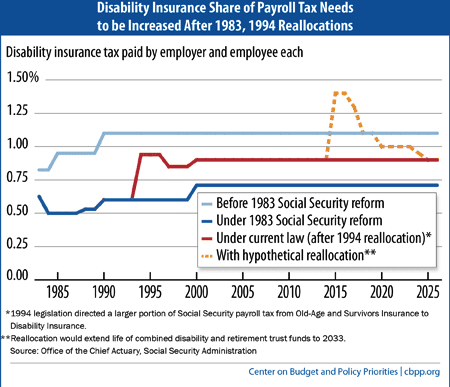

In 1983, Congress adopted several measures to shore up the program, including gradually raising the full retirement age from 65 to 67, increasing the payroll tax, and taxing some of the benefits of higher-income beneficiaries, with the new revenue going into Social Security’s trust fund.

Current proposals to fix Social Security follow a similar trajectory.

Some suggest raising the full retirement age to 69 or 70, or gradually increasing the payroll tax from 6.2% to 7.4%. Bills have been introduced in Congress to raise the cap on the amount of income subject to the payroll tax from the current $128,400.

Other proposals call for revising how cost-of-living adjustments are calculated so that annual benefit increases will be smaller—a change that would affect current and future beneficiaries.

Social Security “is a fixable problem—as long as Congress intervenes before 2034,” says Dan Adcock, director of government relations for the National Committee to Preserve Social Security & Medicare. “Obviously, every year you wait, you have to pay for a larger shortfall in the program.”

Higher Payouts

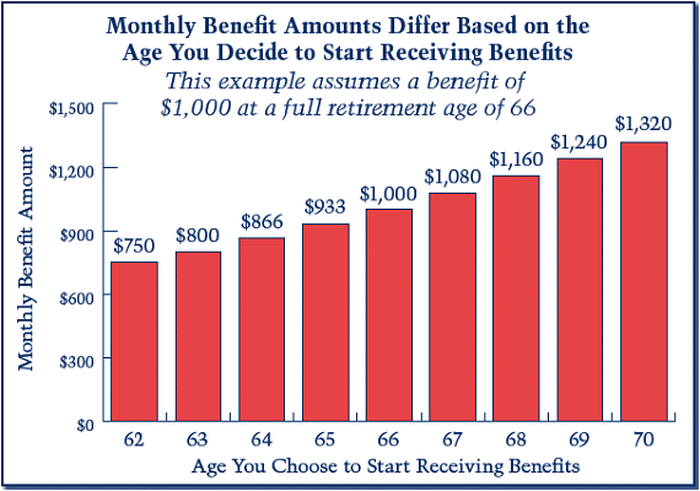

Some individuals who are in poor health have no choice but to file for benefits at age 62. But if you do, your benefits will be permanently reduced by 25% to 30%. If you’re married, claiming early could also reduce spousal and survivor benefits for your partner.

If you’re working or have other sources of income, it’s almost always better to wait until at least full retirement age, which is 66 if you were born between 1943 and 1954 and gradually rises to 67 for people born after 1960.

Source: Social Security Administration, Motley Fool

Delaying benefits beyond that means your payout will grow by 8% a year until age 70.

Delaying benefits also increases the value of annual cost-of-living adjustments because they’ll be compounded on a higher base. The Social Security trustees report estimates a 2.4% increase for 2019, the largest adjustment in seven years.

Sources:

Finacial Media Exchange

Social Security Administration

The Motley Fool

Center on Budget and Policy Priorities

WSJ