U.S. stocks hit new record highs as the prospects for a wider armed conflict between the U.S. and Iran faded by the end of the week.

Technology stocks outperformed as bellwether Apple reported stronger-than-expected iPhone sales in China. The tech-heavy NASDAQ Composite rose for a fifth consecutive week, adding 1.8%, while the large cap S&P 500 gained half that at 0.9%.

The Dow Jones Industrial Average rose 189 points ending the week at 28,823—a gain of 0.7%.

Smaller cap benchmarks finished the week in the red with both the S&P 400 mid cap index and Russell 2000 small cap index giving up -0.2%.

International Markets: Canada’s TSX rose 1.0%, while the United Kingdom’s FTSE gave up -0.5%. Markets on Europe’s mainland were mixed. France’s CAC 40 retreated -0.1%, while Germany’s DAX jumped 2.0%. In Asia, China’s Shanghai Composite rose 0.3% and Japan’s Nikkei gained 0.8%.

As grouped by Morgan Stanley Capital International, developed markets rose 0.3% and emerging markets gained 1.5%.

Commodities: Precious metals finished the week mixed. Gold added 0.5% to end the week at $1560.10 an ounce, but Silver gave up -0.3% to close at $18.10 an ounce. After five consecutive weeks of gains, oil finished the week down a sizeable -6.4% to $59.04 per barrel for West Texas Intermediate crude.

The industrial metal copper, viewed by some analysts as a barometer of world economic health due to its variety of uses, retraced most of last week’s decline by rising 1.0%

US Economic Trends

The jobs market ended 2019 on a sour note as December’s payroll and wage growth both missed expectations. The Labor Department’s Non-Farm Payrolls report (NFP) showed nonfarm payrolls increased by just 145,000. Economists had expected a reading of 160,000.

Furthermore, average hourly earnings rose by just 2.9%, missing the 3.1% projection.

December marked the first time that wage gains were below 3% on an annualized basis since July of 2018. The unemployment rate remained at 3.5% – a 50-year low. In the details, services payrolls rose 140,000 led by retail trade (+41k), leisure and hospitality (+40k), and health care (+28k). Goods-producing payrolls edged down 1,000, as a 20,000 job increase in construction was completely offset by declines in manufacturing (-12K) and mining-and-logging (-9K).

Following the release, analysts noted the report was consistent with policy makers’ expectations and expect no change in monetary policy. A bright spot in an otherwise lackluster report was the broader measure of unemployment, known as the U6 component of the NFP report. The U6 measures not only unemployed but also marginally employed and involuntarily part time workers. It came in at a new record low of 6.7%, beating the previous low of 6.8% set back in October of 2000.

The number of Americans seeking first-time unemployment benefits fell for a fourth week in a row as new jobless claims fall back to a near 50-year low. The Labor Department reported initial jobless claims declined by 9,000 last week to 214,000. The reading was below economists’ forecasts of 220,000. The less-volatile monthly average of new claims dropped by 9,500 to 224,000. Overall, the trend appears to have flattened since the spring of 2019 and remains close to its lowest level since 1973.

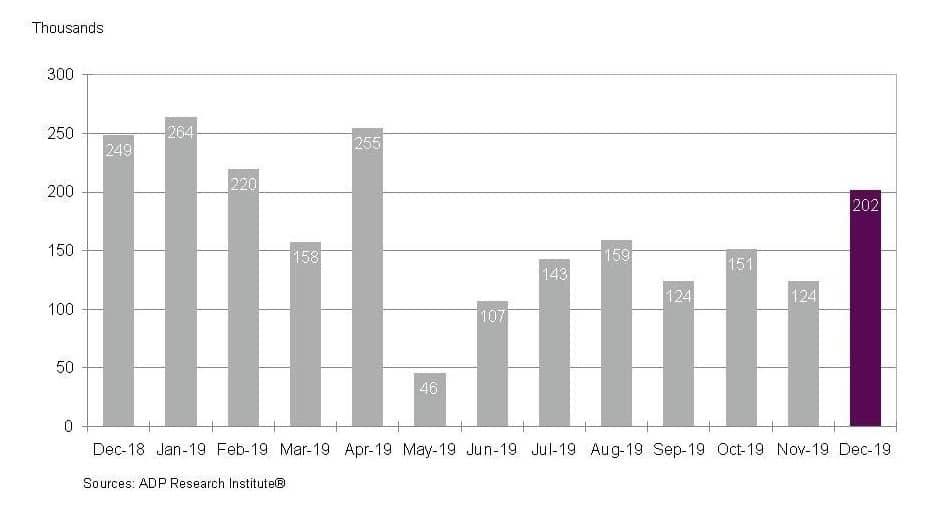

In contrast to the NFP report, payroll-processor ADP reported that the private sector added the most jobs in over half a year. ADP reported private payrolls increased 202,000 in December. Analysts had expected an increase of just 150,000.

ADP reported that the private sector added the most jobs in over half a year

Despite the strong performance at the end of the year, hiring moderated over the course of the year. Private payrolls increased an average of 163,000 per month in 2019—down from 219,000 in the previous year. In the report, services payrolls increased 173,000 led by a jump of 78,000 in the trade/transportation/utilities category.

Goods-producing payrolls rose by 29,000—all of it in construction. Payroll gains were concentrated in small and medium-sized firms, which together accounted for ¾ of the total increase.

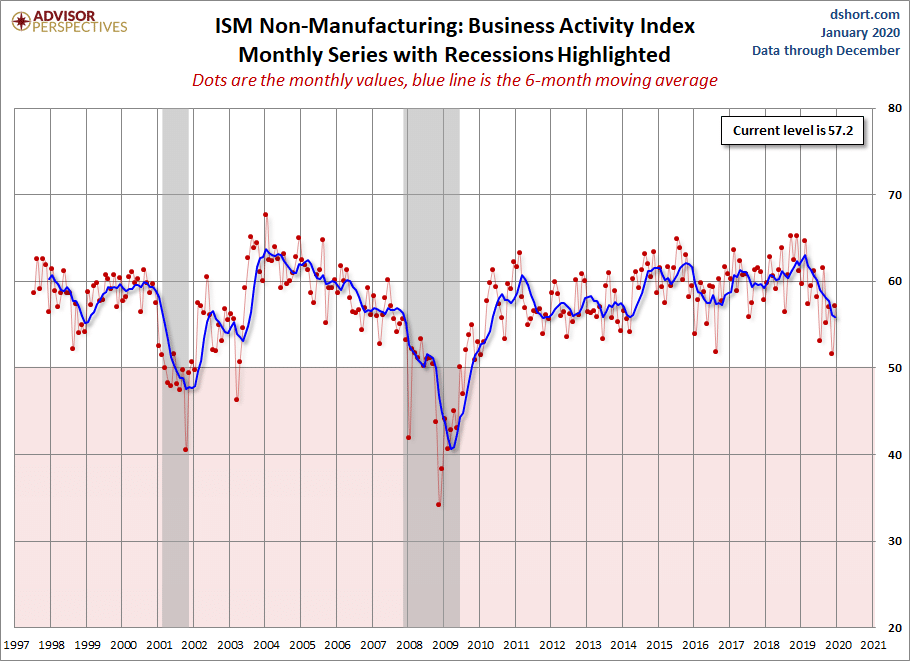

The services side of the economy, responsible for roughly 80% of the overall U.S. economy, rose to a four-month high at the end of 2019, the Institute for Supply Management (ISM) reported. ISM stated its nonmanufacturing index rose 1.1 point to 55 in December.

Economists had expected a reading of 54.3. Readings over 50 indicate growth, while readings at 55 or above are considered exceptional. Anthony Nieves, chairman of the services survey stated, “The respondents are positive about the potential resolution on tariffs.”

In the details, the increase was led by a 5.6 point jump in business activity to 57.2—its best level since August. Furthermore, 11 of the 17 industries tracked by ISM said their businesses were expanding.

In a related survey, analytics firm Markit reported its U.S. services Purchasing Managers’ Index (PMI) also rose in December. That index also hit a five-month high, lifted by new orders and employment growth.

Long Term Market Valuations

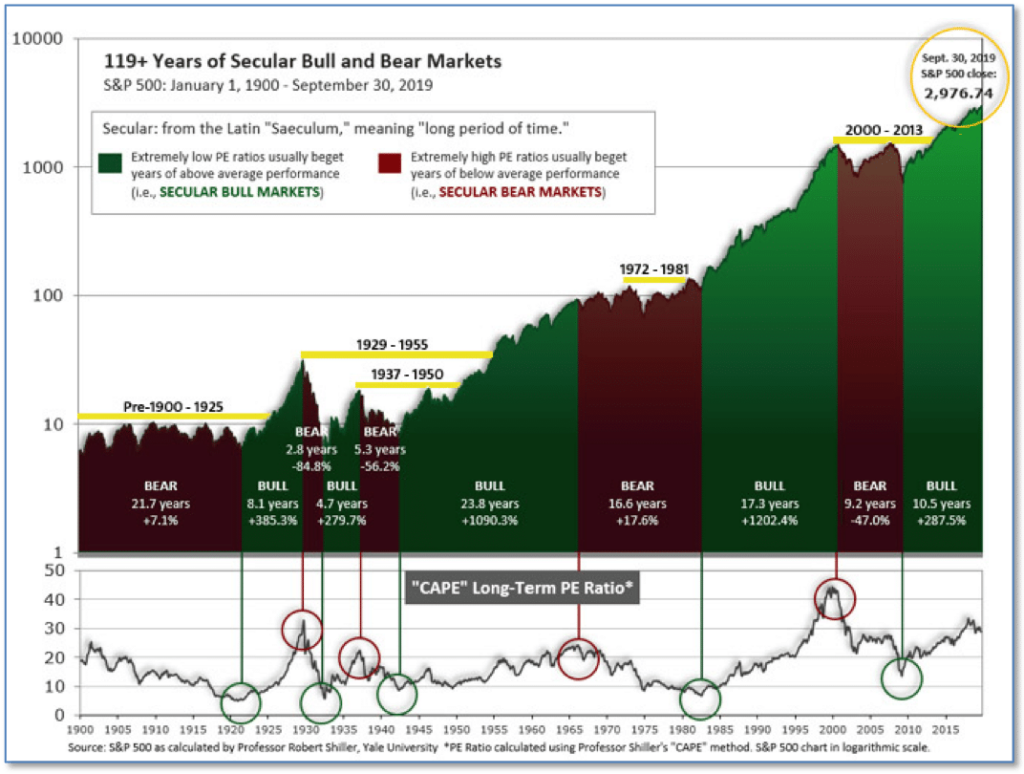

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that increases in market prices only occur in a general response to earnings increases, instead of rising “just because”). The market is currently at that level.

Figure 1 – 100-year view of Secular Bull and Bear Markets

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind as buyers rush in to buy first and ask questions later. Two manias in the last century – the 1920’s “Roaring Twenties” and the 1990’s “Tech Bubble” – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid and the following decade or two are spent in Secular Bear Markets, giving most or all of the mania gains back.

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 31.31, up from the prior week’s 31.02, above the level reached at the pre-crash high in October, 2007. Since 1881, the average annual return for all ten year periods that began with a CAPE around this level have been in the 0% – 3%/yr. range. (see Fig. 2).

Figure 2 – Historical CAPE Range

Riverbend Technical Indicators

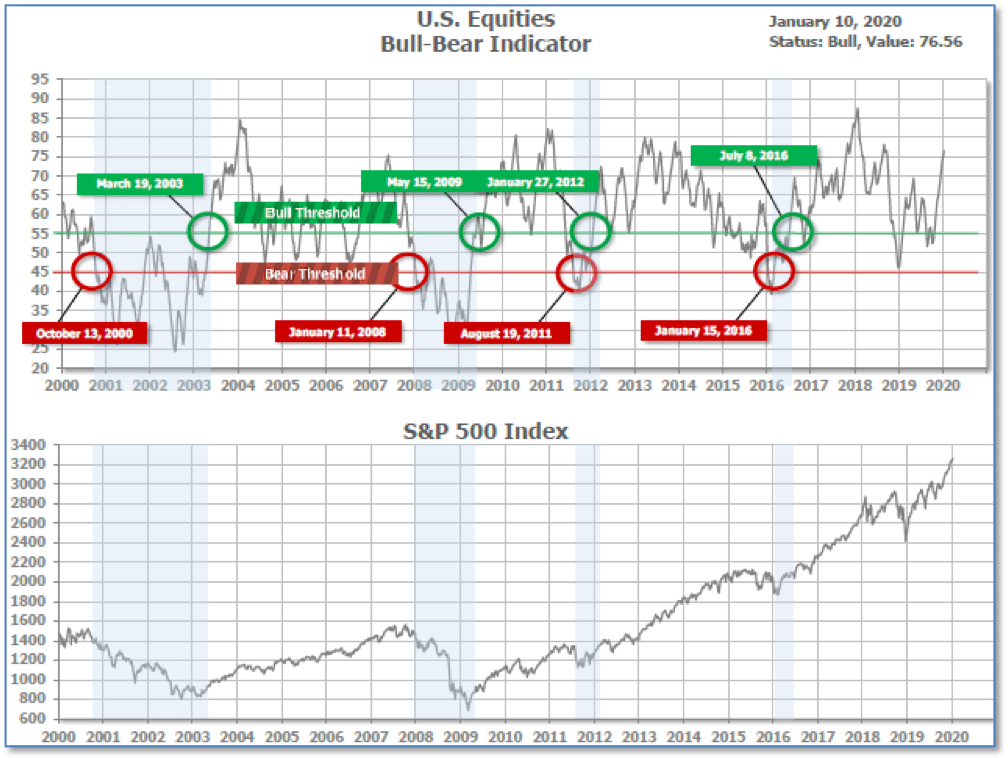

We view long term market cycles as months-to-years timeframe – the timeframe in which Cyclical Bulls and Bears operate. The U.S. Bull-Bear Indicator (see Fig. 3) is in Cyclical Bull territory at 76.56, up from the prior week’s 75.04.

Figure 3 = Long Term Bull-Bear Indicator: US Equities

Intermediate And Short-Term Picture:

The Shorter-term (weeks to months) Indicator (see Fig. 4) is positive. The indicator ended the week at 33, up 1 from the prior week’s 32

Separately, the Intermediate-term Quarterly Trend Indicator – based on domestic and international stock trend status at the start of each quarter – was positive entering October, indicating positive prospects for equities in the fourth quarter of 2019.

Figure 4 – Short Term Indicator: US Equities

SHUT vs DIME

The ranking relationship (shown in Fig. 5) between the defensive SHUT (“S”=Staples [a.k.a. consumer non-cyclical], “H”=Healthcare, “U”=Utilities and “T”=Telecom) and the offensive DIME sectors (“D”=Discretionary [a.k.a. Consumer Cyclical], “I”=Industrial, “M”=Materials, “E”=Energy), is one way to gauge institutional investor sentiment in the market.

The average ranking of Defensive SHUT sectors dropped to 14.25 from the prior week’s 13.50, and the average ranking of the Offensive DIME sectors rose slightly to 20.00 from the prior week’s 20.25.

The Defensive SHUT sectors lost a bit of their lead over the Offensive DIME sectors

Note: these are “ranks”, not “scores”, so smaller numbers are higher ranks and larger numbers are lower ranks.

Figure 5 – Riverbend US Asset Class Rankings

Figure 5 – Riverbend US Asset Class Rankings

Summary

In the Secular (years to decades) timeframe (Figs. 1 & 2), the long-term valuation of the market is historically too and favors actively managed investment strategies. The Bull-Bear Indicator (months to years) remains positive (Fig. 3), indicating a potential uptrend in the longer timeframe.

In the intermediate timeframe, the Quarterly Trend Indicator (months to quarters) is positive for Q1, and the shorter (weeks to months) timeframe (Fig. 4) is positive.

Therefore, with three indicators positive and none negative, the U.S. equity markets are rated as Positive.

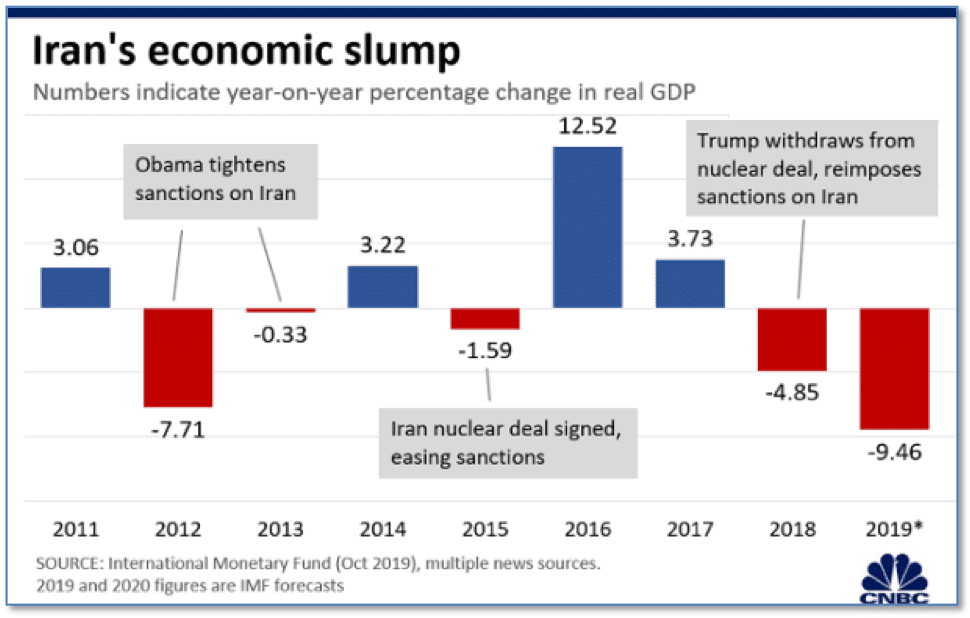

Interesting Chart of the Week

Following America’s killing of top Iranian general Qasem Soleimani in an airstrike, Iran responded with a missile barrage on U.S. interests in Iraq. Some feared war was inevitable, and Google searches for “World War III” spiked.

However, officials from both countries have insisted they’re not interested in seeking an all-out war. Despite the humanitarian costs a war would bring to both countries, economists have pointed out the main reason Iran isn’t interested in a conflict is simple: it can’t afford it.

With inflation running at more than 30%, curtailed oil exports, and a dramatically shrinking GDP (see chart below from cnbc.com), Iran is in no position to take on the financial burden of a war with the US or any other major power.