[fusion_builder_container hundred_percent=”no” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” overlay_color=”” video_preview_image=”” border_size=”” border_color=”” border_style=”solid” padding_top=”” padding_bottom=”” padding_left=”” padding_right=””][fusion_builder_row][fusion_builder_column type=”1_1″ layout=”1_1″ background_position=”left top” background_color=”” border_size=”” border_color=”” border_style=”solid” border_position=”all” spacing=”yes” background_image=”” background_repeat=”no-repeat” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”0px” margin_bottom=”0px” class=”” id=”” animation_type=”” animation_speed=”0.3″ animation_direction=”left” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” center_content=”no” last=”no” min_height=”” hover_type=”none” link=””][fusion_text]

The very big picture (a historical perspective):

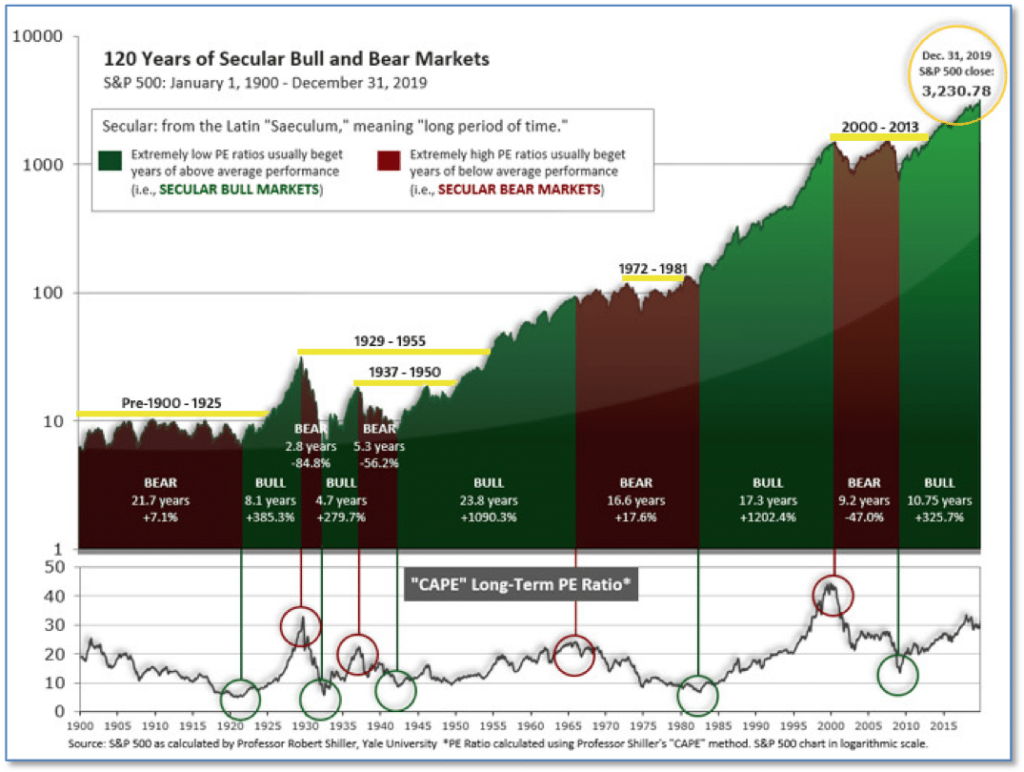

The long-term valuation of the market is commonly measured by the Cyclically Adjusted Price to Earnings ratio, or “CAPE”, which smooths-out shorter-term earnings swings in order to get a longer-term assessment of market valuation. A CAPE level of 30 is considered to be the upper end of the normal range, and the level at which further PE-ratio expansion comes to a halt (meaning that further increases in market prices only occur as a general response to earnings increases, instead of rising “just because”). The market was recently at that level.

Of course, a “mania” could come along and drive prices higher – much higher, even – and for some years to come. Manias occur when valuation no longer seems to matter, and caution is thrown completely to the wind – as buyers rush in to buy first, and ask questions later. Two manias in the last century – the “Roaring Twenties” of the 1920s, and the “Tech Bubble” of the late 1990s – show that the sky is the limit when common sense is overcome by a blind desire to buy. But, of course, the piper must be paid, and the following decade or two were spent in Secular Bear Markets, giving most or all of the mania-gains back.

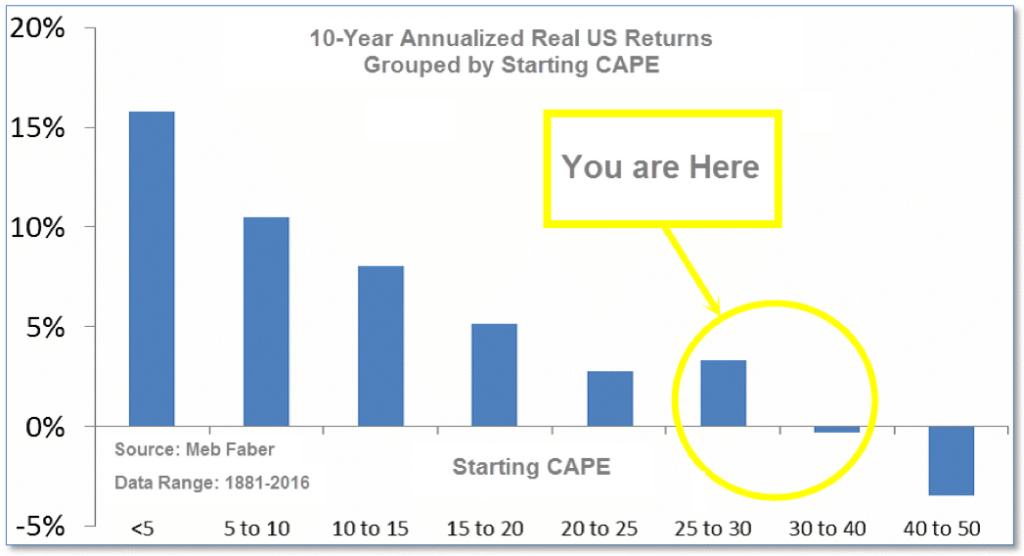

See Fig. 1 for the 100-year view of Secular Bulls and Bears. The CAPE is now at 25.71, down from the prior week’s 28.22. Since 1881, the average annual return for all ten-year periods that began with a CAPE around this level have been flat to slightly-negative (see Fig. 2).

Note: We do not use CAPE as an official input into our methods. However, if history is any guide – and history is typically ‘some’ kind of guide – it’s always good to simply know where we are on the historic continuum, where that may lead, and what sort of expectations one may wish to hold in order to craft an investment strategy that works in any market ‘season’ … whether current one, or one that may be ‘coming soon’!

The big picture:

As a reading of our Bull-Bear Indicator for U.S. Equities (comparative measurements over a rolling one-year timeframe), we remain in Cyclical Bull territory.

The complete picture:

Counting-up of the number of all our indicators that are ‘Up’ for U.S. Equities the current tally is that three of four are Positive, representing a multitude of timeframes (two that can be solely days/weeks, or months+ at a time; another, a quarter at a time; and lastly, the {typically} years-long reading, that being the Cyclical Bull or Bear status).

In the markets:

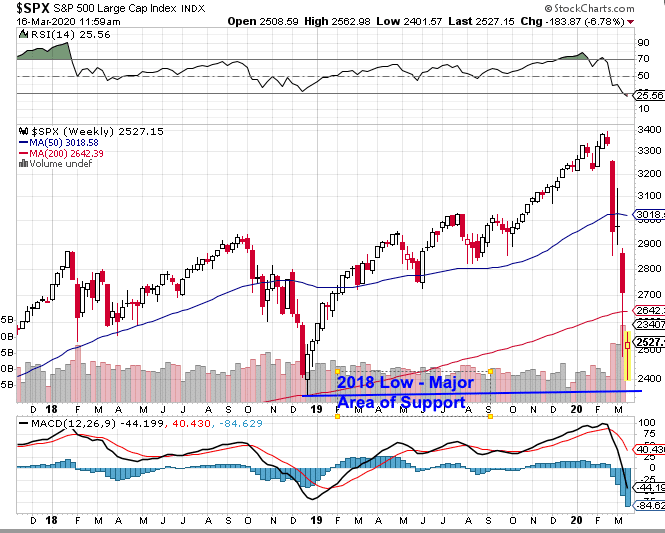

U.S. Markets: Stocks suffered a week of historic losses as worries deepened about the effects of the coronavirus outbreak, compounded by a destructive price war in the oil industry. During the week, the declines pushed the major indexes well into bear market territory, with the Dow Jones Industrial Average falling over 28% from its recent peak to its Thursday low, and the S&P 500 Index down about 27% as of Thursday’s close. The onset of the bear market was the fastest in history, by a long shot.

Major indexes were setting new highs as recently as mid-February – and the Dow suffered its worst daily decline since 1987 on Thursday. Trading “circuit breakers”, designed to halt trading when the S&P 500 falls by more than 5% and then 7% were triggered on both Monday and Thursday for the first time since 1997. Despite the late-day rally on Friday, the Dow Jones Industrial Average finished the week down 2679 points to 23,185 – a decline of -10.4%.

The technology-heavy NASDAQ Composite, likewise, gave up 700 points, a loss of -8.2%. By market cap, the large cap S&P 500 experienced a decline of -8.8%, while the mid cap S&P 400 and small cap Russell 2000 plunged a much larger ‑14.0% and ‑16.5%, respectively.

International Markets: International markets were also a sea of red, and mostly worse than the US. Canada’s TSX declined -15.2%, while the United Kingdom’s FTSE 100 retreated -17.0%. On Europe’s mainland, France’s CAC 40 and Germany’s DAX each plunged ‑20.0%, while Italy’s Milan FTSE plummeted -23.3%.

In Asia, China’s Shanghai Composite lost -4.9%, while Japan’s Nikkei ended down -16.0%. As grouped by Morgan Stanley Capital International, developed markets fell -14.3%, while emerging markets ended down -10%.

Commodities: Precious metals, normally viewed as a safe-haven during times of distress, failed to live up to expectations this week. Gold plunged -9.3% to $1516.70 per ounce, while silver plummeted -16.0% to $14.50 per ounce.

Energy continued to sell off for a third week. West Texas Intermediate crude oil declined a whopping -23% to just $31.73 per barrel – its lowest price since early 2017. The industrial metal copper retraced all of last week’s gain, finishing down -3.8%. Copper is viewed by some analysts as a barometer of global economic health due to its wide variety of uses.

U.S. Economic News: The number of Americans that applied for first-time unemployment benefits last week fell slightly, remaining near a 50-year low. The Labor Department reported initial jobless claims dropped by 4,000 to 211,000 in the week ended March 7.

Economists had expected a reading of 220,000. New jobless claims are being watched closely for early signs of damage to the economy from the coronavirus. They are likely to rise soon if falling sales force companies to lay off more workers. The more stable monthly average of jobless claims edged up 1,250 to 214,000.

The four-week figure filters out the weekly ups and downs to give a better sense of labor-market trends. The total number of people already collecting unemployment benefits declined by 11,000 to 1.72 million. These claims had soared to as high as 6.6 million near the end of the 2007-2009 recession.

Sentiment among the nation’s consumers tumbled in March as fears over the coronavirus continue to grow. The University of Michigan reported its consumer sentiment index fell 5.1 points to 95.9—its weakest reading in five months. The index is almost certainly guaranteed to fall more sharply in the months ahead. The current reading only covered the first 11 days of March, right before the bad news about the coronavirus epidemic pushed the U.S. into crisis mode. Jim Curtin, chief economist of the survey stated, “The data suggest that additional declines in confidence are still likely to occur as the spread of the virus continues to accelerate.” In addition, Ian Shepherdson, chief economist at Pantheon Economics stated, “If past experience is any guide, we should expect [sentiment] to fall by a further 15 to 25 points over the next couple of months.”

The cost of living increased slightly last month according to the latest data from the Bureau of Labor Statistics (BLS). The BLS reported its consumer price index ticked up 0.1% in February; economists had expected the reading to be unchanged. Over the past year, the increase in the cost of living slipped to 2.3% from 2.5%. The level of inflation remains low by historical standards, and economists expect the even relatively tame price pressures to wane soon.

In the details, the cost of food rose 0.4%, the biggest increase in a year, while rents increased 0.3%. Prices also rose for clothes, used vehicles, education, car insurance and medical care. The cost of energy, mostly gas, declined. Energy is expected to fall even further as Russia and Saudi Arabia have both ramped up production in their ongoing price war.

Another closely-watched measure of inflation that strips out food and energy, the so-called “core rate”, increased 0.2% last month. The yearly increase in the core rate edged up to 2.4% after sitting at 2.3% for four months in a row.

At the producer level, the cost of goods and services posted its biggest decline last month in five years, mostly due to the plunge in oil prices. The Bureau of Labor Statistics reported its Producer Price Index (PPI) sank 0.6% last month. Economists had predicted just a 0.1% decline. Over the past 12 months, wholesale inflation has risen just 1.3%, and that number is likely to taper off even more if the economic effects of the coronavirus persist. In the details, the cost of goods dropped almost 1% last month, with three-fifths of the decline traced to lower energy prices.

The cost of gasoline fell 6.5% and jet fuel dropped 16.5%, among other things. Wholesale food prices also fell sharply last month, down 1.6%. That’s the biggest drop since 2015. Core PPI, which strips out food, energy and trade margins, ticked down 0.1% last month. Over the past 12 months, the core rate edged down to 1.4% from 1.5%. Lydia Boussour, economist at Oxford Economics wrote in a note to clients, “Looking ahead, the disinflationary impact from the virus and the crash in oil prices will exert even more downward pressure on prices.”

Chart of the Week:

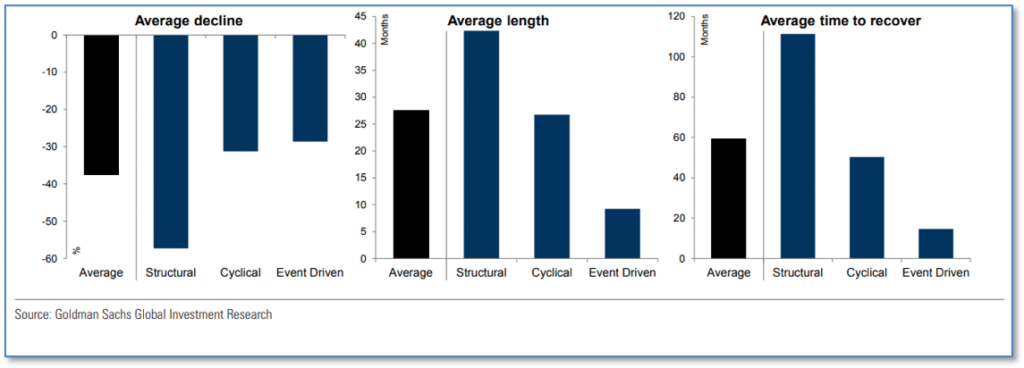

Goldman Sachs analyst Peter Oppenheimer analyzed bear markets going all the way back to 1835 and classified them as either “structural”, “cyclical” or “event-driven”. Through his research, Oppenheimer had some good news and some bad news about the current slump.

First the bad: “Event-driven” bear markets, such as the current coronavirus pandemic, on average, result in 29% declines. That’s bad, considering that we’re not to that level yet.

The good news, Oppenheimer says, is that such bear markets generally regain their previous levels within 15 months. The other two types of bear markets, structural and cyclical, generally see drops of 57% and 31%, respectively, and take much longer to recover.

What I am Watching

The US equity markets are extremely oversold. In my view, investors have been worried about two items:

- Liquidity – this was resolved by a massive rate cut from the Fed last night.

- Action from Washington – we are still waiting on this. The markets would like to see a bipartisan economic package that will help support individuals impacted. Something similar to the bailouts we had in 2008 – but instead of the banks, this time it needs to be the consumer.

Once these two items are in place, we should start having a recovery from oversold levels.

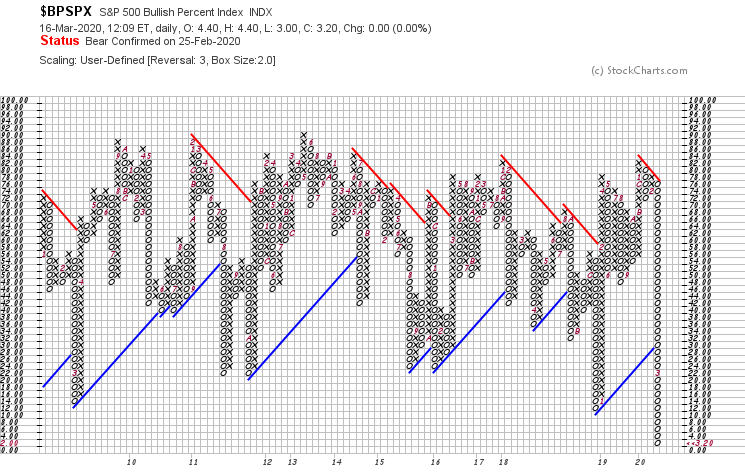

The NYSE Bullish % Index is at historically low levels:

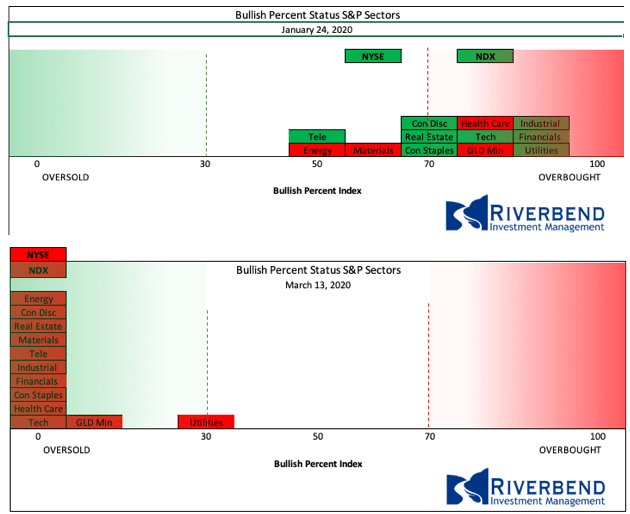

Additionally, individual sectors are very, very oversold:

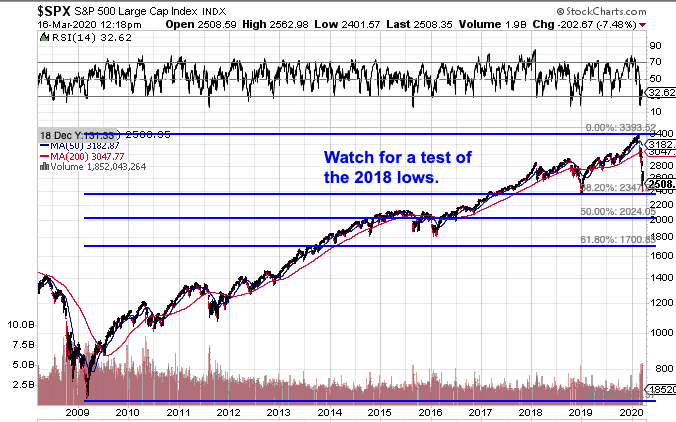

For now, keep an eye on the 2018 lows. If we start trading below those levels, I think we will need to start discussing how much of the 2009-2020 Bull Market we are about to give back.

(Sources: All index- and returns-data from Yahoo Finance; news from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet.)

[/fusion_text][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container]