However, like any theory, MPT is not without its criticisms and instances of failure.

Understanding Modern Portfolio Theory (MPT)

At its core, MPT is about maximizing returns for a given level of risk, or conversely, minimizing risk for a given level of expected return.

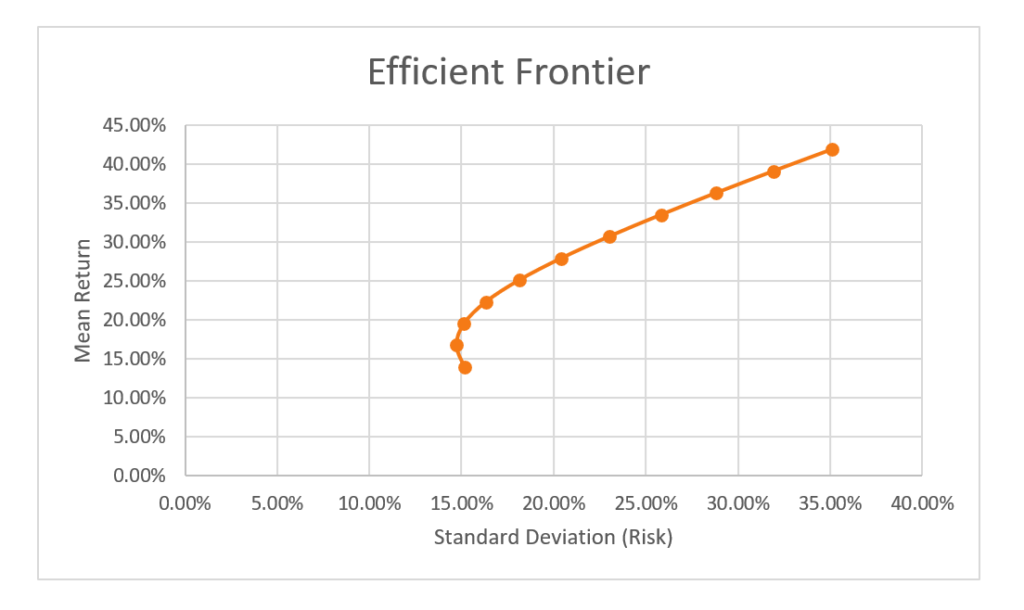

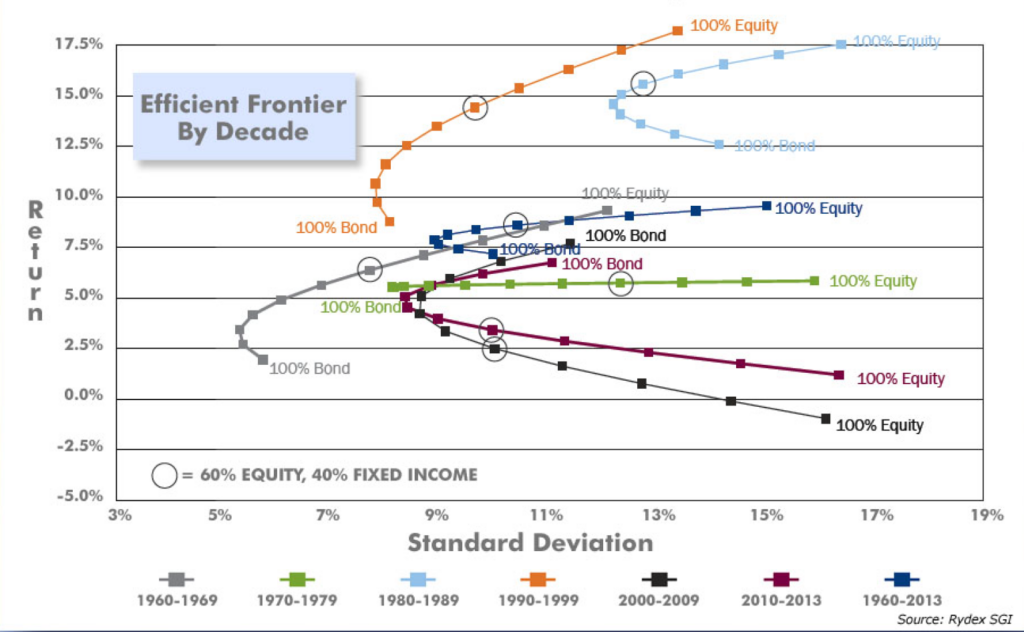

MPT introduces the concept of the “efficient frontier,” a graphical representation of the most efficient portfolios that offer the highest expected return for a given level of risk. These portfolios are deemed optimal because they are expected to provide the best possible returns without taking on unnecessary risk.

Criticisms of Modern Portfolio Theory

Despite its widespread adoption and Nobel Prize-winning acclaim, MPT has faced significant criticism over the years. Critics argue that the theory’s foundational assumptions often do not hold true in the real world, leading to potential misapplications and failures.

- Assumption of Normal Distribution: MPT assumes that returns on assets are normally distributed, which is often not the case. Financial markets are prone to extreme events that can lead to skewed distributions of returns, making the normal distribution assumption unrealistic.

- Static and Simplistic Assumptions: The theory assumes that risk, return, and correlation coefficients are static and can be accurately estimated, which is rarely the case in dynamic financial markets. This can lead to portfolios that are not truly optimized for the current market conditions.

- Underestimation of Systemic Risk: MPT focuses on diversifying away unsystematic risk but often underestimates systemic risk, which cannot be diversified away. This was evident during the 2008 financial crisis and COVID when correlated declines across asset classes led to significant portfolio losses, challenging the effectiveness of diversification.

- Overreliance on Historical Data: MPT relies heavily on historical data to estimate future returns, volatilities, and correlations. However, past performance is not always indicative of future results, leading to potential misestimations and suboptimal portfolio construction.

Examples of MPT Failures

- 2008 Financial Crisis: The global financial crisis of 2008 is often cited as a significant failure of MPT. During the crisis, the correlations between asset classes increased dramatically, leading to widespread portfolio losses. This event highlighted the limitations of MPT in predicting and mitigating systemic risk.

- Dot-com Bubble: The burst of the dot-com bubble in the early 2000s also challenged MPT’s effectiveness. Many investors who diversified across technology stocks found that their portfolios were not protected against the sector-wide downturn, underscoring the theory’s limitations in the face of market irrationality and sector-specific risks.

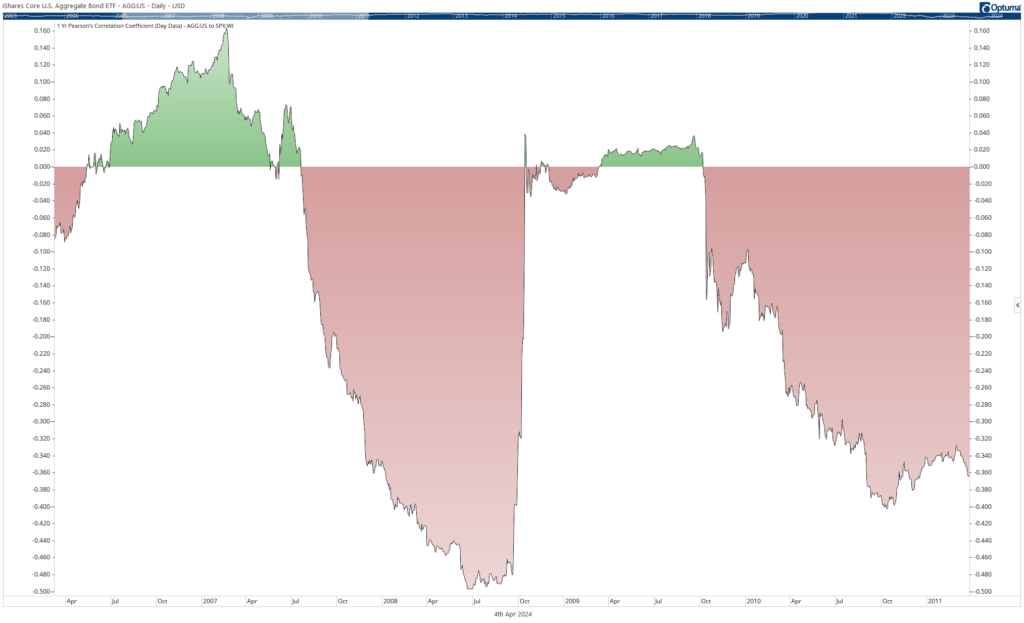

The correlation between stocks and bonds rapidly changed during the 2008 Financial Crisis

The correlation between stocks and bonds rapidly changed during the 2008 Financial Crisis

While Modern Portfolio Theory has fundamentally changed investment strategy and portfolio management, it is not without its flaws. The theory’s assumptions often do not align with the complexities of real-world financial markets, leading to potential misapplications and failures.