Strong strategic wealth management habits pay off throughout life. Yet, with age, it is probable that your specific, financial goals are likely to change.

Life cycle planning identifies both common goals and investment strategies for the key stages of adult life. This knowledge can help you when examining and reassessing your particular portfolio requirements.

Starting Out

Between the ages 25 to 35, common financial goals often include: saving for a down payment on a first home, establishing a college fund for young children, and putting away funds for retirement.

However, financial goals often create competition for perhaps limited income resources.

Therefore, it is imperative that you spend the time necessary to rank your financial goals in order of importance.

For example, do you slow down saving for a home in order to put enough money away for a child’s education needs?

With a longer planning horizon, you may have the opportunity to enhance your investment returns through the effects of compound interest, tax-deferred growth, and, possibly, a relatively high-risk tolerance.

Compound Interest Over Time

Starting Value: $10,000

Interest Rate: 8%

[table “10” not found /]

To secure a comfortable retirement at this stage, you would do well to start saving as early as possible.

You should consider contributing the maximum to an employer-sponsored plan, such as a 401(k) plan. Many companies match all, or portions, of employee contributions, which will further enhance long-term results.

If you do not participate in an employer-sponsored plan, consider an Individual Retirement Account (IRA). Your contributions to a traditional IRA may be tax deductible, and earnings are tax-deferred.

Contributions to a Roth IRA are not tax-deductible, but earnings grow tax-deferred and distributions are tax-free, provided you are at least age 59½ and have owned the account for at least five years.

It is important to follow a diversified investment strategy that conforms to your long-range retirement planning goals. A well-diversified retirement portfolio will have assets placed in different types of investments and investment classes that cover a wide range of the risk/return spectrum.

Examples of some investment vehicles include: stocks, bonds, mutual funds (which can include stocks, bonds, or a combination of both), certificates of deposit (CDs), savings, and money market accounts.

Each investment class tends to react differently to changes in financial markets and to the economy as a whole. By diversifying your portfolio, you spread risk over a broader range of investments, potentially minimizing the impact of downturns in the economy or a particular market sector.

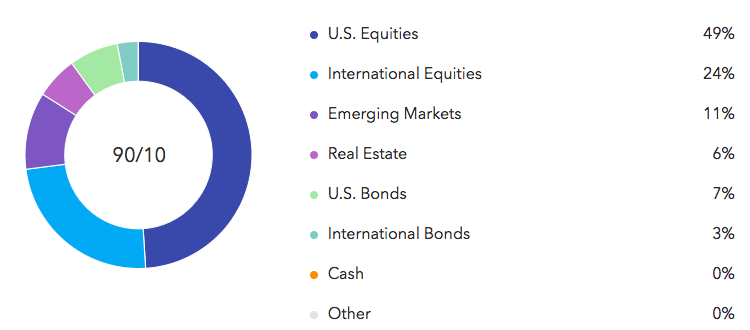

When determining how to allocate assets as part of an overall strategic wealth management strategy, younger individuals may be better positioned to think “growth” by emphasizing equities.

An Example of an Aggressive Growth Strategy*

Source: Right Capital, Riverbend Investment Management

Although common stocks generally tend to be riskier than other investments, over the long run—say, 25 years—they have historically yielded higher returns.

Of course, investment returns and principal values of stocks and stock mutual funds will fluctuate due to market conditions. Therefore, when shares are redeemed, they may be worth more or less than their original cost.

It is important to keep an eye on the “big picture” when it comes to asset allocation. Looking at the big picture means incorporating all assets (such as personal savings, home equity, and retirement plan funds) when determining the best investment mix.

Your Peak Earning Years

Between the ages of 35 to 55, saving for a child’s college education often becomes a higher priority. As earnings increase, you may want to “trade up” to a larger home or make another major purchase, such as a vacation home.

Moreover, as the years pass, the need to boost retirement savings becomes a more pressing reality.

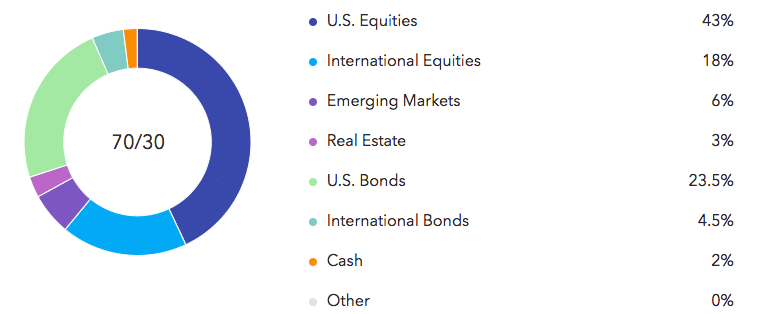

The key to a solid investment approach may be to continue to take advantage of the potential growth produced by an equity-dominated portfolio.

An Example of a Growth Strategy*

Ultimately, it may be wise to gradually begin introducing income investments. Bond or stock and bond funds may help produce valuable income that can be used to help pay for a child’s college expenses or to help diversify a portfolio.

With personal income at its height, it is also important to maximize tax-deferred qualified plan contributions and take advantage of the tax benefits offered by annuities and tax-exempt securities.

Nearing Retirement

Between the ages of 55 to 65, the emphasis is generally on safeguarding accumulated assets.

Another goal is to reduce overall debt—such as from college expenses or a mortgage—to take advantage of extra discretionary income to help increase retirement savings.

As your planning horizon shortens, the watchwords are “asset preservation.”

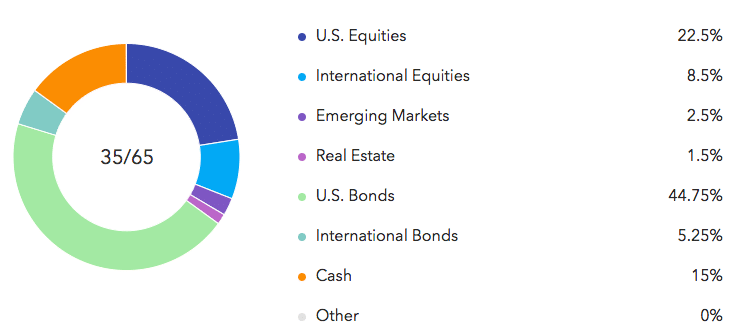

An Example of a Conservative Allocation*

A typical portfolio strategy involves shifting a larger portion of assets from equities to more conservative fixed-income securities to achieve a better balance between growth and income.

Income mutual funds, bond funds, and annuities can all play important roles in balancing your portfolio.

If your earnings remain high, attention should also be given to help reduce tax obligations.

This may be accomplished by adding tax-free bond funds to the investment mix. You may want to allocate assets for grandchildren, or consider the benefits of gifting.

Your Retirement Years

After age 65, your primary financial focus may be on generating a steady income stream and protecting it from the effects of inflation and taxes.

As your salary or wages decrease or stop, investments must produce sufficient income to help supplement Social Security and pension benefits.

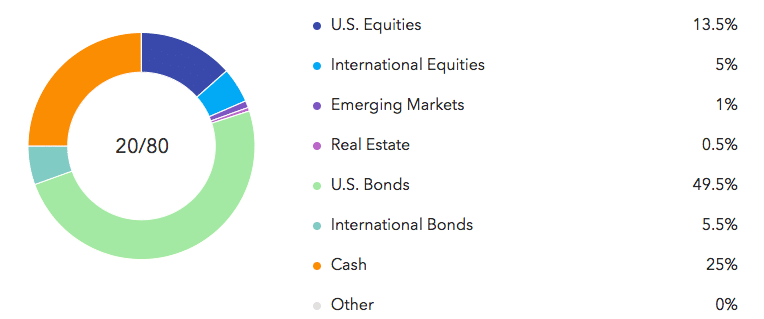

In a strategic wealth management plan, a retiree’s portfolio should place a greater emphasis on income-generating stock and bond funds and annuities.

However, growth stocks and mutual funds should not be entirely discounted.

An Example of A Capital Preservation Allocation*

Growth-type investments can still serve a useful purpose in the battle against inflation, providing a measure of portfolio sustainability.

Also, with the increased life expectancies of individuals today, retirees may still have a long-term investment horizon for a good portion of their savings.

Taxes may still remain an issue if you are a retiree with a particularly high income. If so, tax-free bonds can help reduce tax obligations.

Strategic Wealth Management and Securing the Future

The life cycle approach can play an important role in helping you chart a course to financial success.

By understanding the needs that are common at different life stages, you may be in a better position to choose the most appropriate savings and investment strategies for your situation. Always remember that investing involves risk.

There are never any iron-clad guarantees. And, while past performance is informative, it can never be studied with the assumption that historical profits will mean similar gains in the future.

Therefore, it is the actual knowledge of how investments work and what potential benefits they can provide that will help you determine your ability to accept the risks and, hence, sleep more comfortably each night.

*Sample only, not customized for any client/reader. Please consult a financial professional to determine the proper allocation based on age, risk tolerances, and financial goals.

This site is for educational and informational purposes only. Nothing contained here should be construed by anyone as an invitation or solicitation to buy or sell any security. This site does not contain personalized legal, tax, investment, or financial advice. Users of this site should consult with a qualified adviser to obtain advice suited to their personal circumstances. Any links provided here to other websites are for informational purposes only. We take no responsibility for the accuracy or content of linked sites.

Copyright © 2018 RSW Publishing. All rights reserved. Distributed by Financial Media Exchange.