Market Recap

The first week of the second quarter saw a pullback in U.S. equities, as stronger-than-expected economic data fueled concerns that the Federal Reserve might delay cutting interest rates later in 2024. The major U.S. large-cap equity indices retreated from their recent record highs, while a small flight to safety pushed the 10-year U.S. Treasury yield higher.

Despite the overall market decline, growth stocks outperformed value stocks, and large-caps fared better than smaller companies. Energy stocks continued to shine as oil prices reached another 2024 high, their highest level since October 2023, amid rising geopolitical tensions.

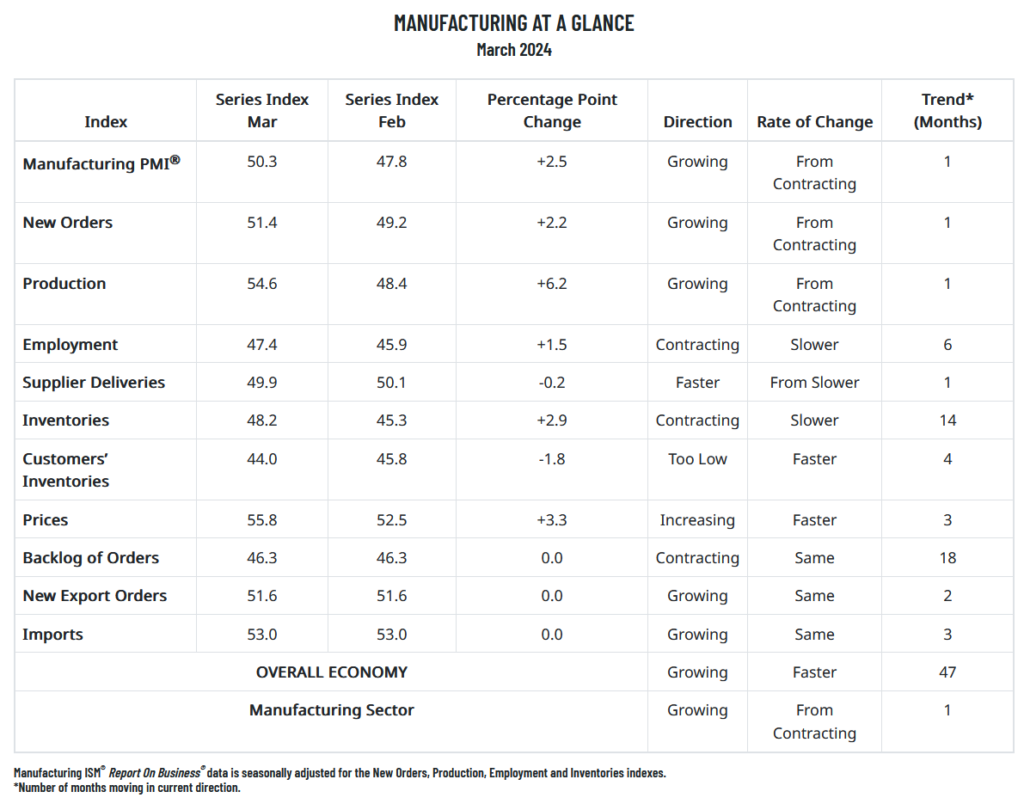

The Institute for Supply Management’s indexes also influenced market sentiment this week. The March ISM manufacturing reading came in well above expectations, indicating expansion for the first time in 16 months. However, the ISM services report, released two days later, eased some worries as the services index fell for the second consecutive month.

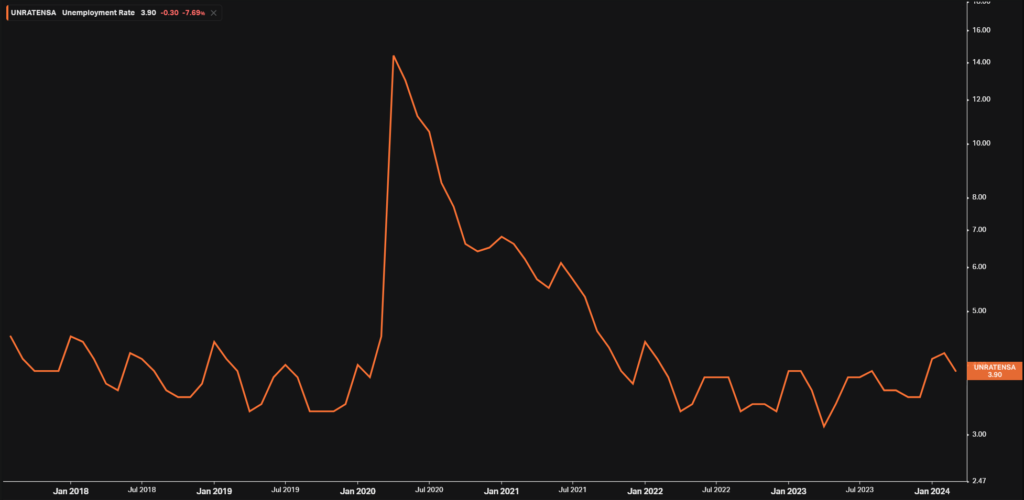

Friday’s jobs report provided a bright spot, showing that the U.S. labor market remains on solid ground. The economy added an impressive 303,000 jobs in March, far exceeding expectations. The unemployment rate remained low at 3.8%, and wage gains were decent. Wall Street interpreted this strong jobs report as a positive sign that the current bull market could continue, despite uncertainty surrounding the timing of the Fed’s rate cuts.

According to the U.S. Bureau of Labor Statistics, job gains occurred in health care, government, and construction sectors. The number of unemployed people remained stable at 6.4 million, and the unemployment rate has been in a narrow range of 3.7% to 3.9% since August 2023. The number of long-term unemployed (those jobless for 27 weeks or more) was little changed at 1.2 million, accounting for 19.5% of all unemployed people.

In other economic news, the U.S. Census Bureau reported that total construction spending in February 2024 was at an annual rate of $2,091.5 billion, 0.3% below January’s $2,096.9 billion. However, this figure is still 10.7% above the February 2023 estimate. During the first two months of 2024, construction spending amounted to $298.1 billion, 11.9% higher than the same period in 2023. Economists polled by Reuters had forecast a 0.7% rebound in construction spending.

As investors continue to monitor economic data and geopolitical developments, the market’s focus will likely remain on the Federal Reserve’s next moves and the potential timing of rate cuts. The strong jobs report may give the central bank more flexibility in its decision-making process, as it aims to strike a balance between controlling inflation and supporting economic growth. For now, the resilience of the U.S. labor market appears to be a key factor in sustaining the ongoing bull market, despite the recent pullback in equities.

Weekly Chart Review

What’s Going On In Your Portfolio?

Our client portfolios continue to focus on value over growth.

Our client portfolios continue to focus on value over growth.

The equity market seems to be finally realizing inflation data is lingering and that the Fed’s rate outlook continues to decrease — something the bond market has been hinting at for a while.

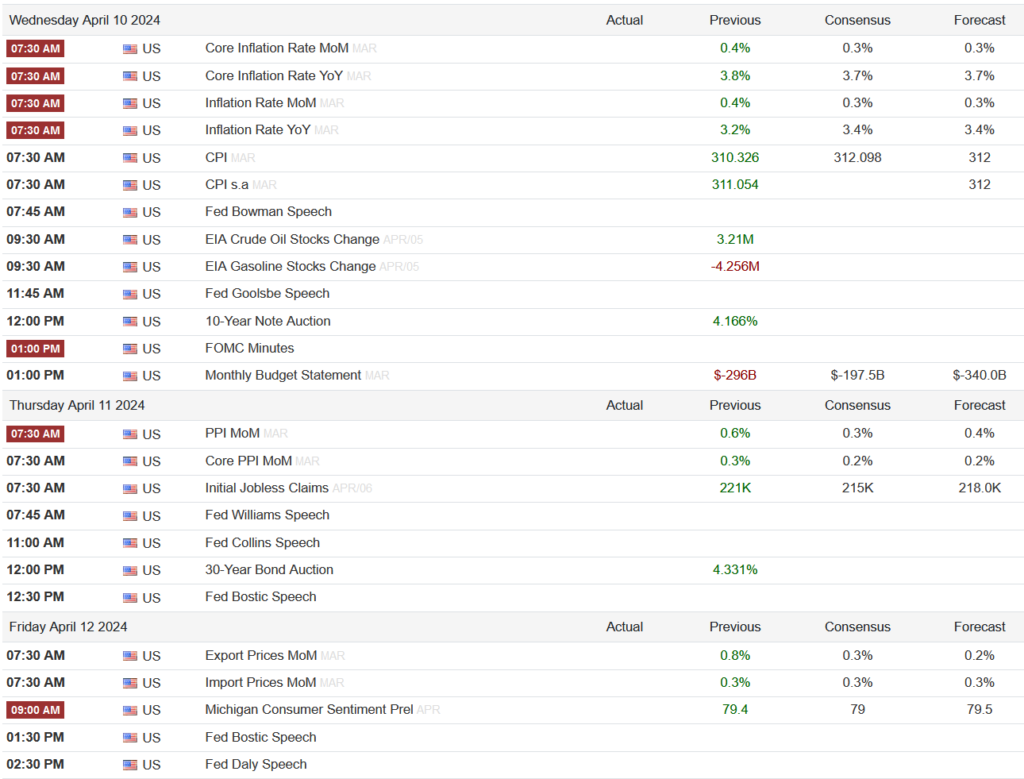

This week there is some key inflation data to keep an eye on, as well as a line of Fed speakers, and the start to earnings season. I will be keeping a close eye on these events, looking for opportunities to reallocate our cash positions.

Upcoming Economic Data to Keep an Eye On

Source: Trading Economics