[fusion_builder_container hundred_percent=”no” equal_height_columns=”no” menu_anchor=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” background_color=”” background_image=”” background_position=”center center” background_repeat=”no-repeat” fade=”no” background_parallax=”none” parallax_speed=”0.3″ video_mp4=”” video_webm=”” video_ogv=”” video_url=”” video_aspect_ratio=”16:9″ video_loop=”yes” video_mute=”yes” overlay_color=”” video_preview_image=”” border_size=”” border_color=”” border_style=”solid” padding_top=”” padding_bottom=”” padding_left=”” padding_right=””][fusion_builder_row][fusion_builder_column type=”1_6″ spacing=”” center_content=”no” link=”” target=”_self” min_height=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” hover_type=”none” border_size=”0″ border_color=”” border_style=”solid” border_position=”all” border_radius=”” box_shadow=”no” dimension_box_shadow=”” box_shadow_blur=”0″ box_shadow_spread=”0″ box_shadow_color=”” box_shadow_style=”” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”” margin_bottom=”” background_type=”single” gradient_start_color=”” gradient_end_color=”” gradient_start_position=”0″ gradient_end_position=”100″ gradient_type=”linear” radial_direction=”center” linear_angle=”180″ background_color=”” background_image=”” background_image_id=”” background_position=”left top” background_repeat=”no-repeat” background_blend_mode=”none” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_type=”regular” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″ last=”no”][/fusion_builder_column][fusion_builder_column type=”2_3″ layout=”1_1″ background_position=”left top” background_color=”” border_size=”” border_color=”” border_style=”solid” border_position=”all” spacing=”yes” background_image=”” background_repeat=”no-repeat” padding_top=”” padding_right=”” padding_bottom=”” padding_left=”” margin_top=”0px” margin_bottom=”0px” class=”” id=”” animation_type=”” animation_speed=”0.3″ animation_direction=”left” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” center_content=”no” last=”no” min_height=”” hover_type=”none” link=””][fusion_text]

[/fusion_text][fusion_vimeo id=”554387044″ alignment=”center” width=”1000″ height=”” autoplay=”false” api_params=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” css_id=”” /][fusion_text]

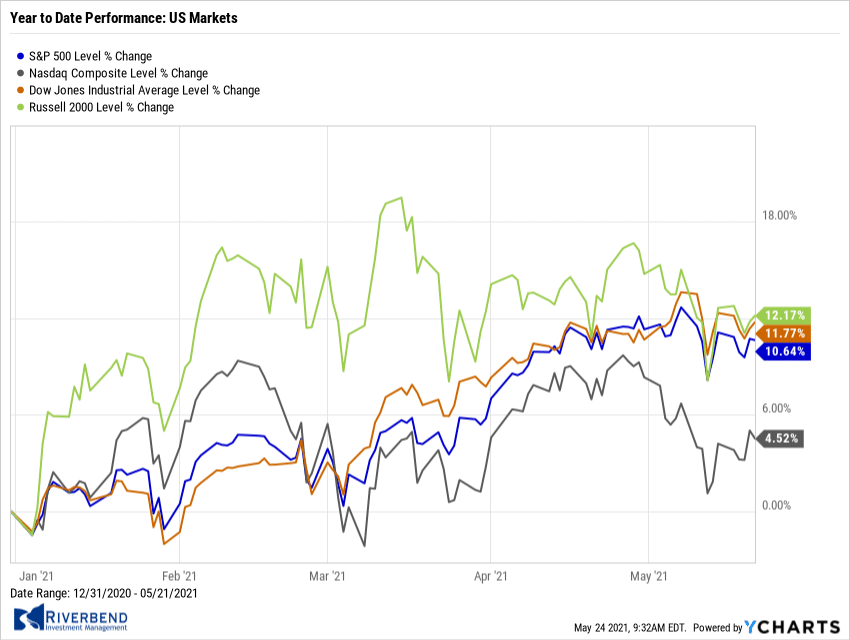

U.S. Markets:

U.S. indices posted mixed results in a volatile week of trading. The large-cap S&P 500 index ended the week modestly lower while the technology-heavy NASDAQ Composite gained a little ground.

The Dow Jones Industrial Average had its second consecutive negative week, declining -0.5% to 34,208. The Nasdaq Composite ended a four week losing streak by finishing the week up 0.3%.

By market cap, the large cap S&P 500 retreated -0.4%, while the mid-cap S&P 400 and Russell 2000 fell -1.2% and -0.4%, respectively.

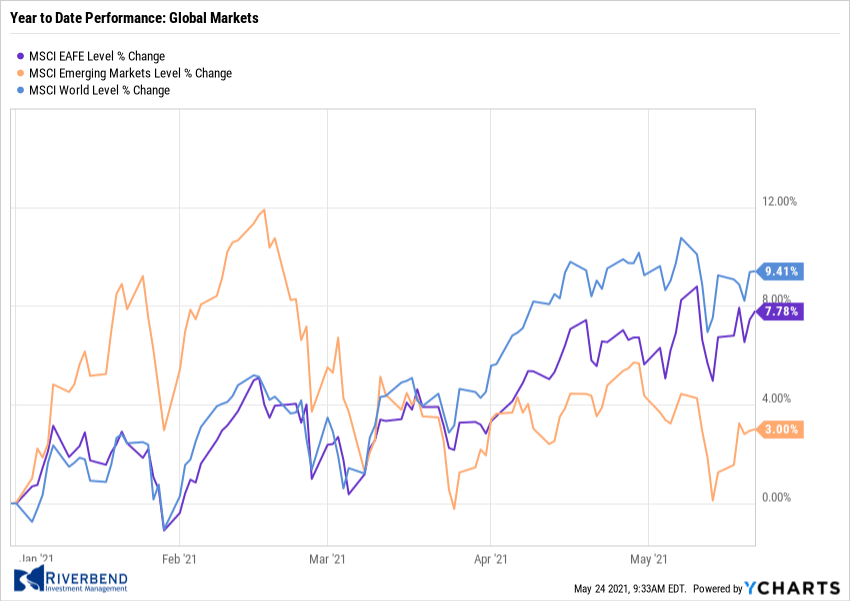

International Markets:

International markets finished the week predominantly to the upside, but with no large moves anywhere.

Canada’s TSX retraced all last week’s decline and then some, rising 0.8%. The United Kingdom’s FTSE 100 closed down for a second week retreating -0.4%.

On Europe’s mainland, France’s CAC 40 finished essentially flat, while Germany’s DAX ticked up 0.1%.

In Asia, China’s Shanghai Composite ticked down -0.1%, while Japan’s Nikkei rose 0.8%.

As grouped by Morgan Stanley Capital International, developed markets ended the week up 0.6% and emerging markets added 0.4%.

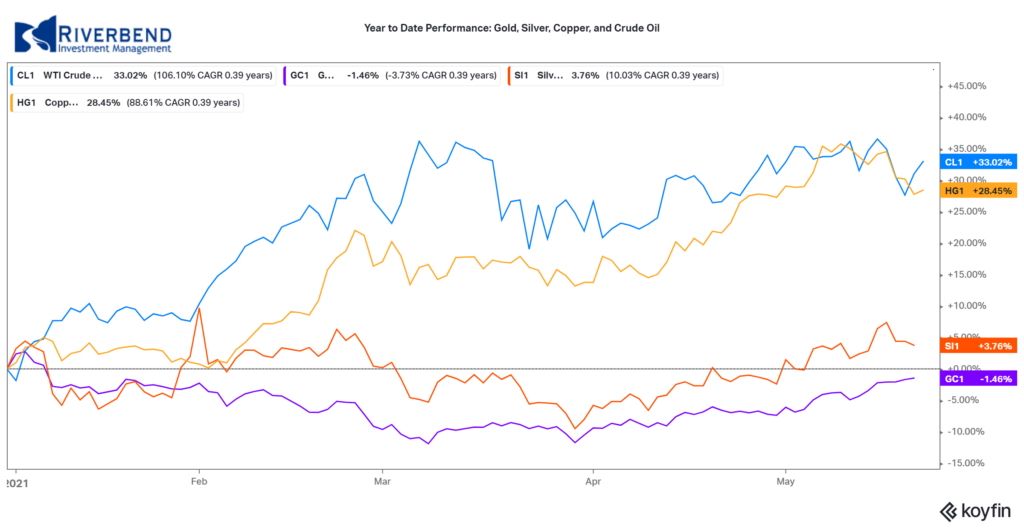

Commodities:

Gold had a third consecutive week of gains, rising 2.1% to $1876.70 per ounce. Silver rose a lesser 0.4% to $27.49 per ounce.

Following three weeks of gains, traders took profits in oil. West Texas Intermediate crude oil finished the week down -2.7% to $63.58 per barrel.

The industrial metal copper, viewed by some analysts as a barometer of world economic health due to its wide variety of uses, finished the week down -3.7%, its second week of declines.

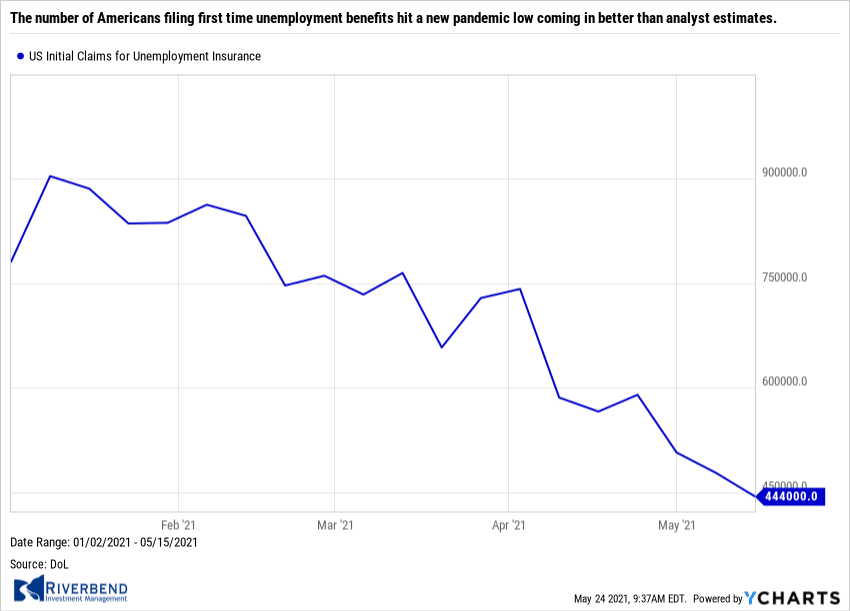

U.S. Economic News:

The number of Americans filing first time unemployment benefits hit a new pandemic low coming in better than analyst estimates. The Labor Department reported initial jobless claims totaled 444,000 last week whereas economists had expected claims to total 452,000. This time last year, claims had totaled more than 2.3 million.

While Federal Reserve officials stress the need for more improvement in the jobs picture, the claims numbers suggest that employment is growing consistently. However, continuing claims, which counts the number of people already receiving benefits, edged higher by rising to 3.75 million. That number is reported with a one-week delay.

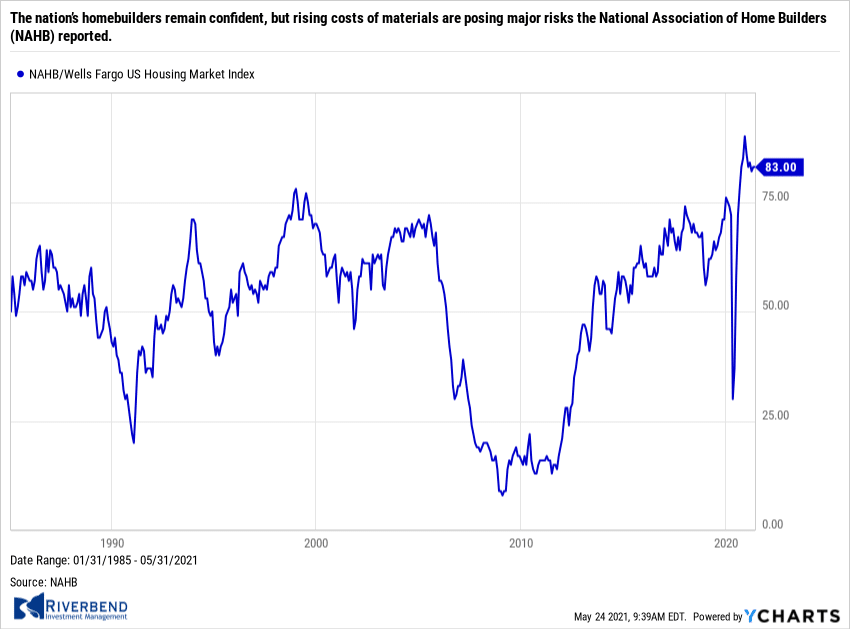

The nation’s homebuilders remain confident, but rising costs of materials are posing major risks the National Association of Home Builders (NAHB) reported. The NAHB said builder sentiment in the single-family housing market remained unchanged at 83 this month. Readings above 50 are considered positive sentiment. The index had plummeted to 37 last May, as the pandemic lockdown hit and the housing market shut down. It then rebounded dramatically in June and July, as consumers rushed to the suburbs seeking more space for working and schooling from home.

The nation’s homebuilders remain confident, but rising costs of materials are posing major risks the National Association of Home Builders (NAHB) reported. The NAHB said builder sentiment in the single-family housing market remained unchanged at 83 this month. Readings above 50 are considered positive sentiment. The index had plummeted to 37 last May, as the pandemic lockdown hit and the housing market shut down. It then rebounded dramatically in June and July, as consumers rushed to the suburbs seeking more space for working and schooling from home.

Builders report strong buyer traffic with continued low mortgage rates helping with affordability, however with prices rising fast they note purchasing power is weakening. “First-time and first-generation homebuyers are particularly at risk for losing a purchase due to cost hikes associated with increasingly scarce material availability,” said Chuck Fowler, National Association of Home Builders chairman. Aggregate residential material costs are now up 12% year over year, according to the NAHB, with some materials – most notably lumber – up much more.

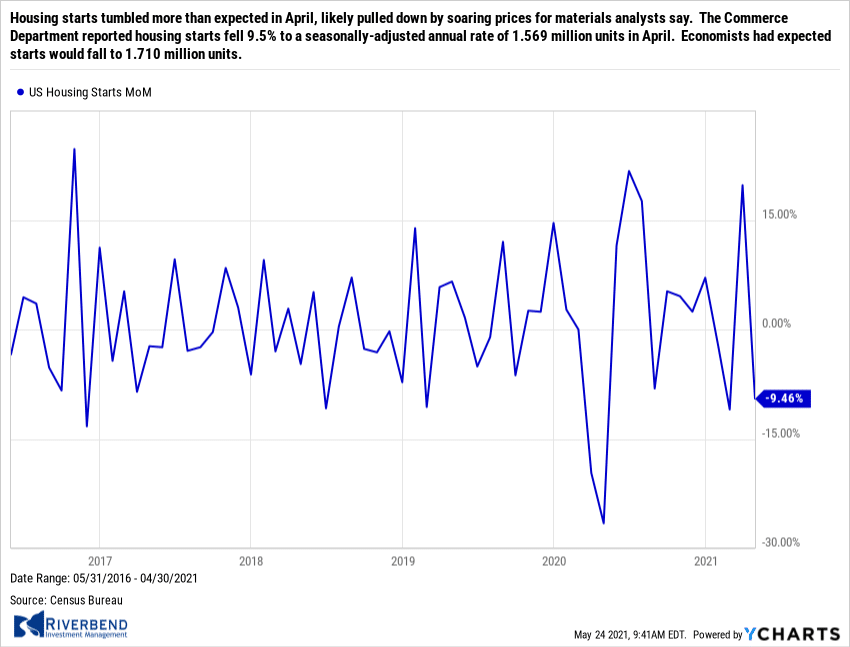

Housing starts tumbled more than expected in April, likely pulled down by soaring prices for materials analysts say. The Commerce Department reported housing starts fell 9.5% to a seasonally-adjusted annual rate of 1.569 million units in April. Economists had expected starts would fall to 1.710 million units. Year-over-year starts were up 67.3% in April.

Housing starts tumbled more than expected in April, likely pulled down by soaring prices for materials analysts say. The Commerce Department reported housing starts fell 9.5% to a seasonally-adjusted annual rate of 1.569 million units in April. Economists had expected starts would fall to 1.710 million units. Year-over-year starts were up 67.3% in April.

Groundbreaking activity dropped in the Midwest and south, but rose in the Northeast and West. Permits for future homebuilding rose 0.3% to a rate of 1.760 million units in April. They soared 60.9% compared to April 2020.

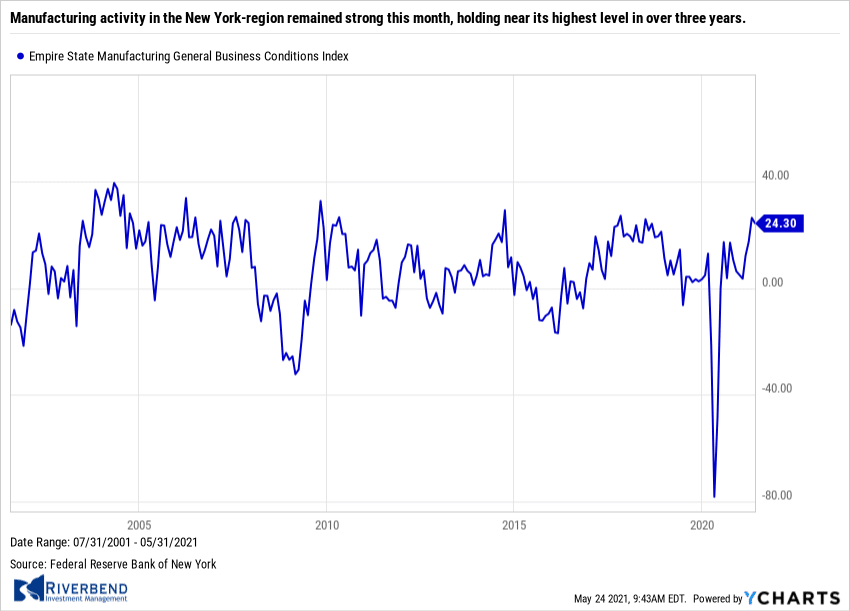

Manufacturing activity in the New York-region remained strong this month, holding near its highest level in over three years. The New York Fed reported its Empire State Manufacturing index down-ticked to a reading of 24.3 in May from 26.3 in April. Economists had expected a reading of 24.8.

Manufacturing activity in the New York-region remained strong this month, holding near its highest level in over three years. The New York Fed reported its Empire State Manufacturing index down-ticked to a reading of 24.3 in May from 26.3 in April. Economists had expected a reading of 24.8.

In the report, the new orders index rose 2 points to 28.9, while shipments rose 4.7 points to 29.7. Both price indices hit record highs. The prices paid index rose 8.8 points to 83.5 while prices received rose 2.2 points to 37.1. On a negative note, expectations for business in the next six months slipped 3.2 points to 36.6. The Empire State reports gets particular attention as it is seen as a leading indicator of national trends.

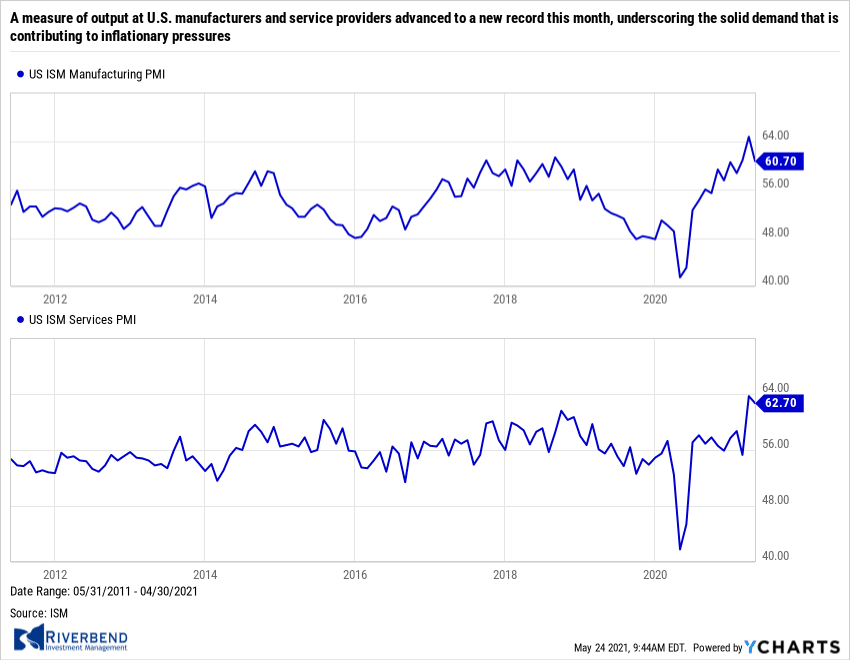

A measure of output at U.S. manufacturers and service providers advanced to a new record this month, underscoring the solid demand that is contributing to inflationary pressures. Data firm IHS Markit said its flash U.S. manufacturing Purchasing Managers Index (PMI) increased 1 point to 61.5 in the first half of this month. That was the highest reading since the survey was expanded to cover all manufacturing industries in October 2009.

A measure of output at U.S. manufacturers and service providers advanced to a new record this month, underscoring the solid demand that is contributing to inflationary pressures. Data firm IHS Markit said its flash U.S. manufacturing Purchasing Managers Index (PMI) increased 1 point to 61.5 in the first half of this month. That was the highest reading since the survey was expanded to cover all manufacturing industries in October 2009.

Economists had forecast the index dipping to 60.2 in early May. A reading above 50 indicates growth in manufacturing, which accounts for 11.9% of the U.S. economy. Booming demand also boosted the services sector, which bore the brunt of the pandemic. The IHS Markit’s flash services sector PMI surged 5.4 points to 70.1—also its highest reading since the series started in October 2009. The services sector accounts for more than two-thirds of U.S. economic activity.

The U.S. LEI suggests the economy’s upward trend should continue and growth may even accelerate in the near term

The Conference Board reported its Leading Economic Index (LEI) had its second consecutive solid gain in April, further evidence that the economic recovery is gathering momentum. The LEI rose 1.6% in April after a 1.3% gain in March. It was the strongest gain since last July. “The U.S. LEI suggests the economy’s upward trend should continue and growth may even accelerate in the near term,” said Ataman Ozyildirim, senior director of economic research at the Conference Board. The index has recovered fully from its COVID-19 contraction. The Conference Board now forecasts real GDP could grow around in a range of 8%-9% in the second quarter, with annual growth expected to reach 6.4%.

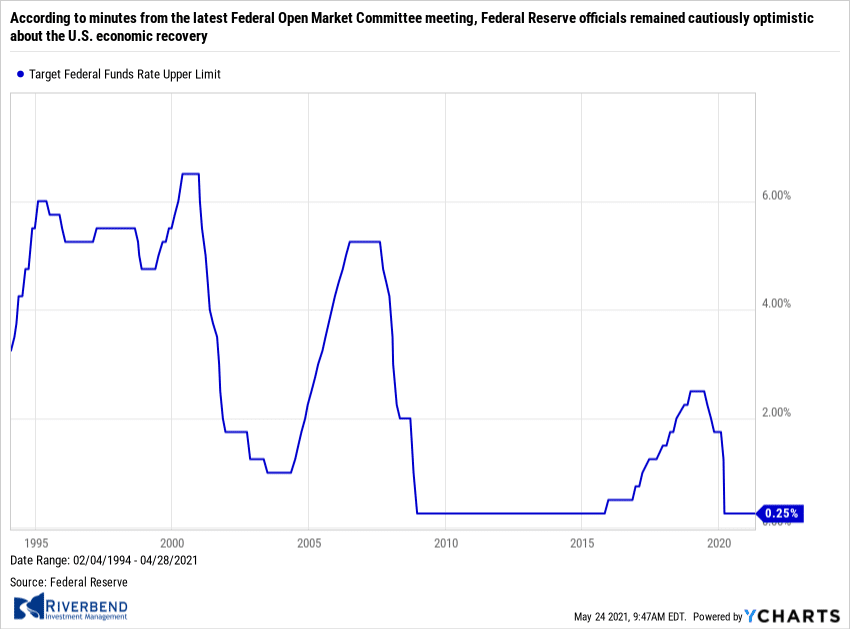

According to minutes from the latest Federal Open Market Committee meeting, Federal Reserve officials remained cautiously optimistic about the U.S. economic recovery. Notes showed some officials signaled they were open to discussing scaling back the central bank’s massive bond purchases “at some point”.

According to minutes from the latest Federal Open Market Committee meeting, Federal Reserve officials remained cautiously optimistic about the U.S. economic recovery. Notes showed some officials signaled they were open to discussing scaling back the central bank’s massive bond purchases “at some point”.

Minutes stated, “A number of participants suggested that if the economy continued to make rapid progress toward the Committee’s goals, it might be appropriate at some point in upcoming meetings to begin discussing a plan for adjusting the pace of asset purchases.” Officials held interest rates near zero at the meeting and pledged to continue buying $80 billion in Treasuries and $40 billion in mortgage-backed securities every month until “substantial further progress” had been made on their employment and inflation goals.

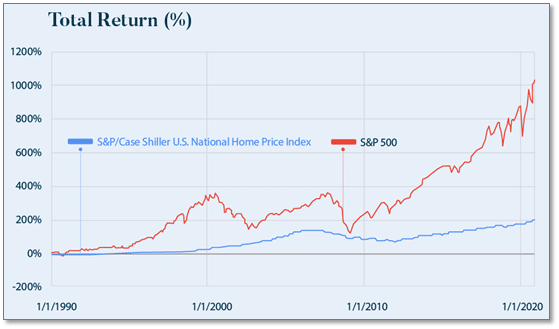

Chart of the Week:

Single-family homes had their biggest price increase on record in the first quarter of this year. With many analysts noting the real estate market is “white hot”, it might be helpful to look at a relative comparison of real estate to the other main source of U.S. homeowner wealth – the stock market.

The above graph from analytics firm Visual Capitalist shows the total return since 1990 of the U.S. National Home Price Index compared to the benchmark S&P 500 stock market index.

The Home Price Index has gone up a respectable 200% since 1990, but looks quite tame compared to the 1000% return from the S&P 500 over the same period.

Riverbend Indicators:

Each week we post notable changes to the various market indicators we follow.

- As a reading of our Bull-Bear Indicator for U.S. Equities (comparative measurements over a rolling one-year timeframe), we remain in Cyclical Bull territory.

- Counting-up of the number of all our indicators that are ‘Up’ for U.S. Equities, the current tally is that four of four are Positive, representing a multitude of timeframes (two that can be solely days/weeks, or months+ at a time; another, a quarter at a time; and lastly, the {typically} years-long reading, that being the Cyclical Bull or Bear status).

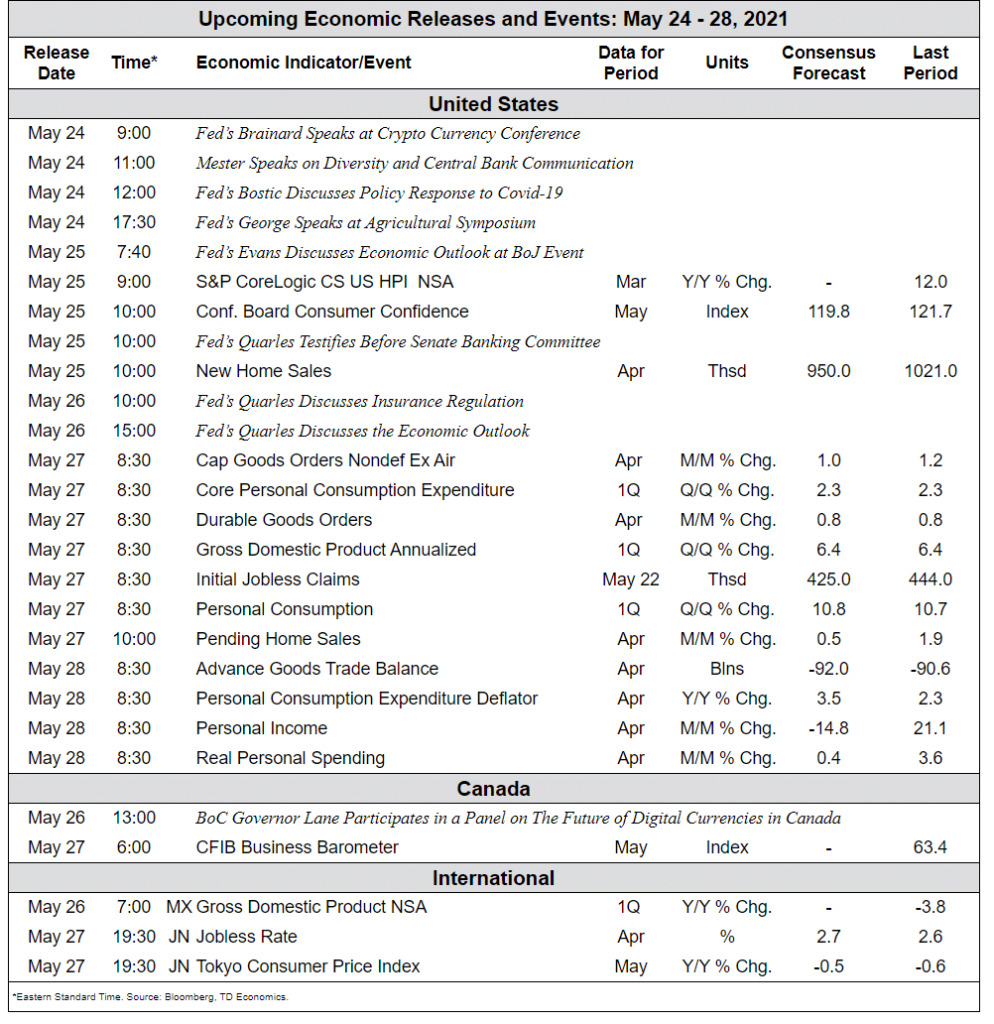

The Week Ahead:

(Sources: All index- and returns-data from Yahoo Finance; news from Reuters, Barron’s, Wall St. Journal, Bloomberg.com, ft.com, guggenheimpartners.com, zerohedge.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com, FactSet.)

[/fusion_text][/fusion_builder_column][fusion_builder_column type=”1_6″ spacing=”” center_content=”no” link=”” target=”_self” min_height=”” hide_on_mobile=”small-visibility,medium-visibility,large-visibility” class=”” id=”” hover_type=”none” border_size=”0″ border_color=”” border_style=”solid” border_position=”all” box_shadow=”no” box_shadow_blur=”0″ box_shadow_spread=”0″ box_shadow_color=”” box_shadow_style=”” background_type=”single” gradient_start_position=”0″ gradient_end_position=”100″ gradient_type=”linear” radial_direction=”center” linear_angle=”180″ background_color=”” background_image=”” background_image_id=”” background_position=”left top” background_repeat=”no-repeat” background_blend_mode=”none” animation_type=”” animation_direction=”left” animation_speed=”0.3″ animation_offset=”” filter_type=”regular” filter_hue=”0″ filter_saturation=”100″ filter_brightness=”100″ filter_contrast=”100″ filter_invert=”0″ filter_sepia=”0″ filter_opacity=”100″ filter_blur=”0″ filter_hue_hover=”0″ filter_saturation_hover=”100″ filter_brightness_hover=”100″ filter_contrast_hover=”100″ filter_invert_hover=”0″ filter_sepia_hover=”0″ filter_opacity_hover=”100″ filter_blur_hover=”0″ last=”no”][/fusion_builder_column][/fusion_builder_row][/fusion_builder_container]