Market Recap

The major U.S. stock indexes posted gains last week, led by the Dow Jones Industrial Average which rose 1.5%. The small-cap Russell 2000 index gained 0.8%, while the large-cap S&P 500 added 0.6%. The tech-heavy Nasdaq Composite ended the week flat.

Despite it being a shortened 4-day trading week due to the Juneteenth holiday on Wednesday, the S&P 500 managed to reach a new record high. Value stocks outperformed growth stocks for a change, and smaller-cap companies beat their larger counterparts.

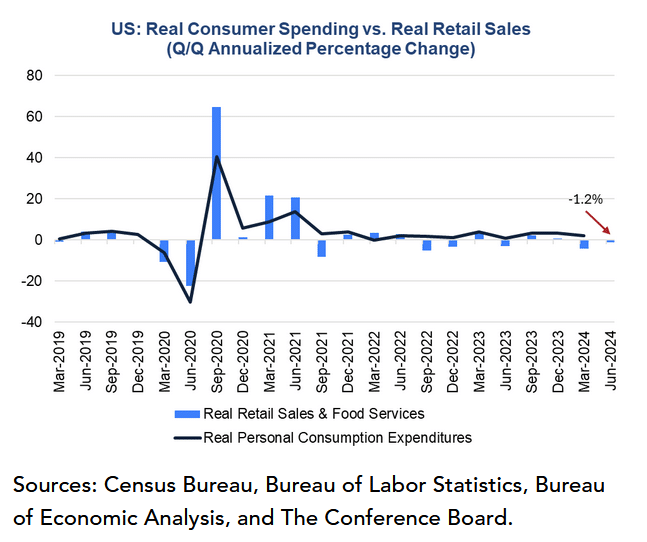

Economic data continues to be mixed. Retail sales barely grew in May, rising just 0.1%, and April’s retail numbers were revised lower. Restaurant and bar sales slipped 0.4%, suggesting consumers are cutting back on discretionary spending.

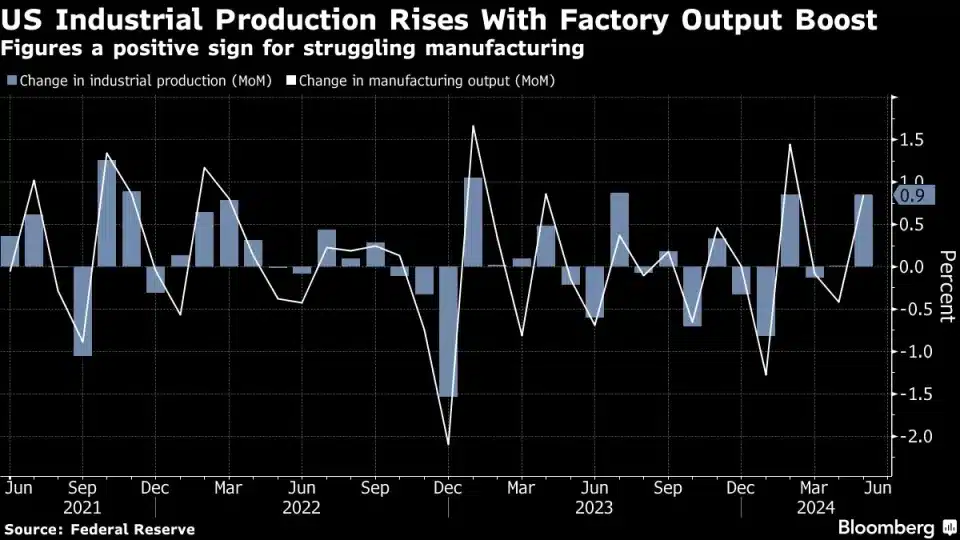

However, manufacturing data was robust. Industrial production jumped 0.9% in May, the biggest gain in about a year. The S&P Global composite business activity index climbed to 54.6 in June, the highest in over two years, signaling solid expansion.

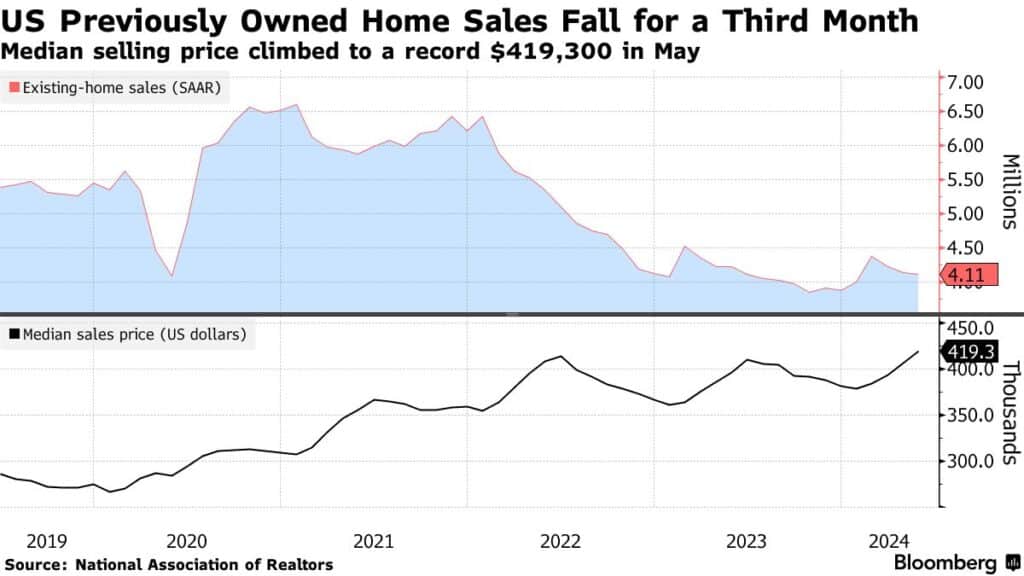

Existing home sales fell 0.7% in May as prices keep climbing. The median existing home price rose 5.8% from a year ago to an all-time high of $419,300, the 11th straight month of annual increases. The median single-family home price was up 5.7% to $424,500.

In other economic news, the Conference Board’s Leading Economic Index (LEI) declined 0.5% in May after a 0.6% drop in April. The LEI has now fallen 2.0% over the past six months, though that’s an improvement from the 3.4% slide in the previous six months. While concerning, the LEI is not currently signaling a recession, according to the Conference Board.

The Week in Charts

What’s Going On In Your Portfolio?

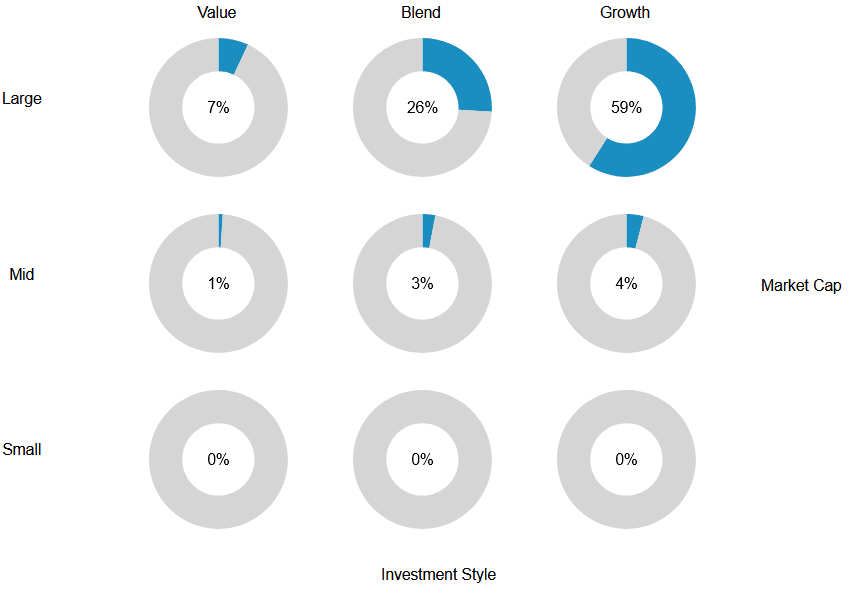

Not much has changed since last week, equity portfolios are currently weighted to favor large-cap growth over value, with little exposure to small and mid-cap stocks.

Seasonal trends plus positive relative strength continue to favor growth names, especially within the technology sector.

As always, volatility stops are in place to help mange any potential downsize risk.

Bond portfolios continue to be fully invested in High Yield bonds, which will benefit from the potential of lower rates in 2025.

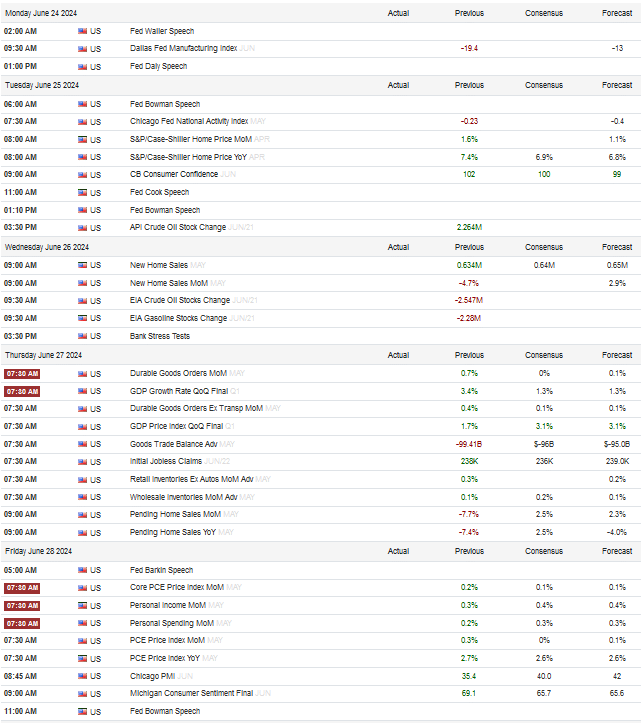

Upcoming Economic Data to Keep an Eye On

Source: Trading Economics